Guest

Топливо против заряда: Переход на электричество дешевле или просто экологичнее?

Создано: 28.07.2025

•

Обновлено: 19.09.2025

Рост числа электрозарядных станций для грузовых автомобилей в Европе привел к переходному периоду на обширных дорожных сетях континента. Для многих операторов автопарков и водителей классические грузовые автомобили на дизельном топливе все еще остаются предпочтительным транспортом. Однако переход на электрические грузовики не за горами, поскольку отрасль продолжает развиваться.

Чтобы оценить целесообразность перехода операторов автопарков с дизельного топлива на электрическое, SNAP провела исследование стоимости подзарядки грузовых автомобилей по сравнению с их заправкой на различных европейских грузовых маршрутах. Мы рассчитали экономию на электричестве по сравнению с дизельным топливом в евро на 100 км в 35 европейских странах.

Мы обнаружили, что Исландия лидирует по этому показателю со средней экономией €61,03 на 100 км, а скандинавские страны Норвегия и Финляндия занимают второе и третье места по экономии соответственно. На другом конце шкалы наименьшая экономия - 19,96 евро на 100 км - в Хорватии, за которой следуют Кипр и Молдова.

В этой статье мы раскрываем экономию затрат по странам Европы и анализируем некоторые из них, а также анализируем некоторые внешние факторы, которые могут повлиять на эту экономию. Мы также рассмотрим, каким может быть будущее eHGV в Европе, а также как eHGV могут помочь операторам автопарков и водителям сэкономить деньги, особенно в случае [бюджетов водителей] (https://snapacc.com/newsroom/a-truck-drivers-guide-to-budgeting/).

Как соотносятся расходы на электромобили и дизельное топливо в странах ЕС

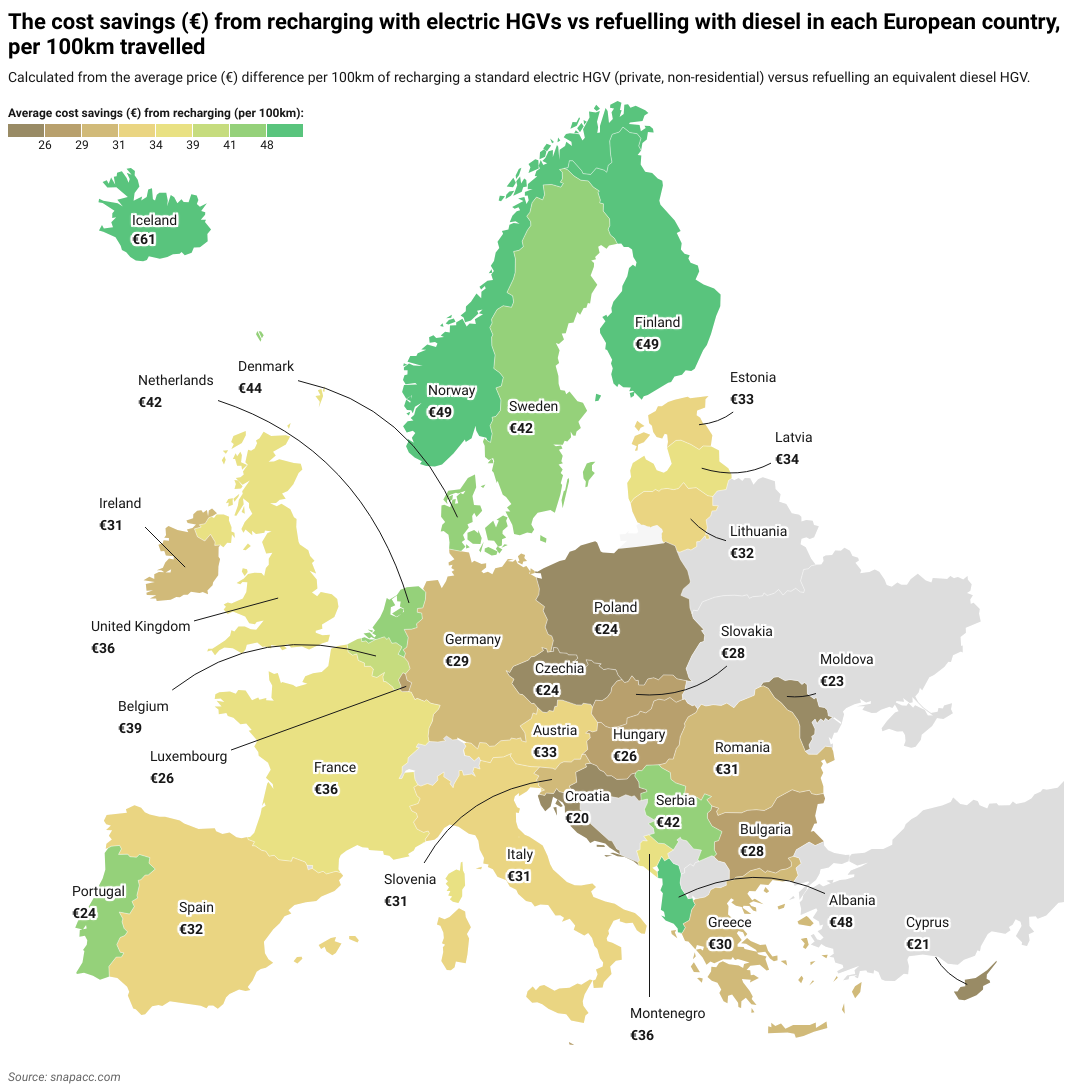

Наше исследование показало, что в каждой европейской стране использование eHGV с электрической зарядкой экономит деньги по сравнению с использованием традиционного грузового автомобиля с топливом. Основное различие заключалось в том, насколько сильно варьировалась экономия. Например, цена на электричество в самой дорогой стране Исландии на 206 % (41 евро) выше, чем в самой дешевой стране, Хорватии.

Мы обнаружили, что в среднем водитель электрического грузового автомобиля экономит 30,59 евро на 100 км по сравнению с водителем дизельного грузового автомобиля. Это означает, что средняя экономия составит 37 200 евро в год для водителей дальних электрогрузовиков и 24 800 евро для водителей внутреннего транспорта.

Чтобы собрать данные, мы рассмотрели 35 европейских стран и сравнили стоимость энергии или топлива на 100 км для двух типов большегрузных автомобилей (HGV). Это были стандартный дизельный грузовик, предполагающий расход топлива 35 литров на 100 км при средней розничной цене дизельного топлива в каждой стране, и электрический грузовик, предполагающий расход электроэнергии 108 кВт/ч на 100 км на основе среднего тарифа на электроэнергию для небытовых потребителей. НДС и возмещаемые налоги были исключены из этих расчетов. Сравнение отражает только прямые затраты "у насоса" или "у розетки", без учета таких факторов, как размер автопарка, заключенные энергетические контракты или будущие изменения цен на топливо и электроэнергию.

При изучении цен на дизельное топливо и электроэнергию использовался ряд источников, включая Eurostat, CEIC, GlobalPetrolPrices, Webfleet и Gov.uk. Стоит отметить, что некоторые из этих источников ссылаются на "Великобританию", а другие - на "Соединенное Королевство". В рамках данного исследования оба термина рассматривались как взаимозаменяемые.

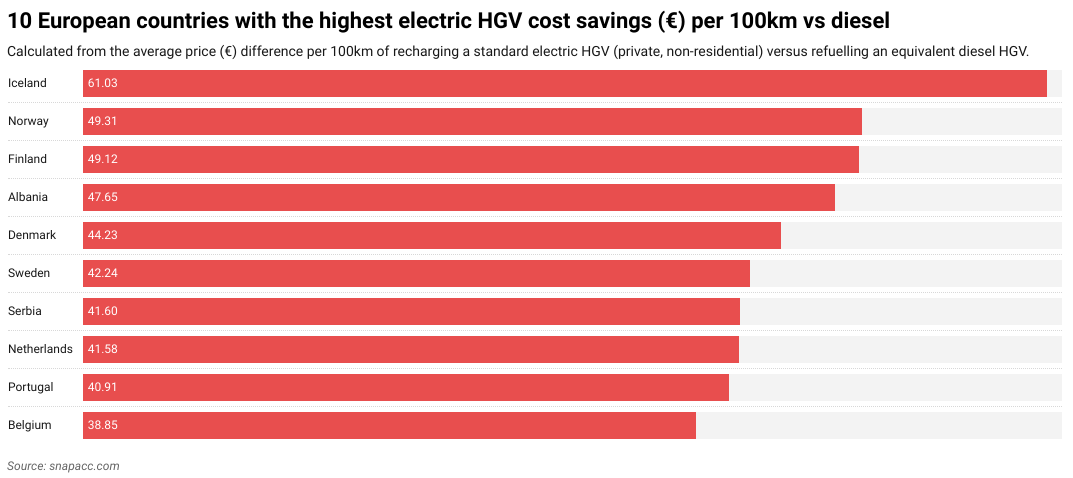

Страны, которые больше всего сэкономят, перейдя на электрические грузовики

Исландия (€61,03), Норвегия (€49,31) и Финляндия (€49,12) - это страны, где можно сэкономить больше всего, перейдя на электрические грузовики.

Во многом это связано с тем, что эти страны входят в число самых дорогих в Европе по цене дизельного топлива. Исландия - самая дорогая страна в Европе по цене дизельного топлива (2,07 евро за литр). Такая высокая стоимость во многом объясняется ее географической изоляцией по сравнению с остальной Европой, в результате чего стоимость импорта дизельного топлива намного выше, чем в других европейских странах. Исландия, как Норвегия и Финляндия, также известна своей высокой налоговой ставкой, что также способствует высокой стоимости топлива.

Норвегия (32%) и Исландия (18%)** также входят в число двух ведущих стран мира по доле электромобилей на дорогах среди легковых автомобилей. В результате обе страны инвестировали значительные средства в инфраструктуру электрозарядок.

Небольшие размеры Исландии и наличие главной кольцевой дороги также облегчают установку электрических зарядных станций на регулярных интервалах для водителей грузовиков с электроприводом. Те же доводы можно частично использовать и для других стран с небольшими сетями, которые отличаются высоким уровнем экономии, включая Албанию, Сербию и Бельгию, хотя следует отметить, что во всех трех странах также действуют одни из самых дорогих цен на дизельное топливо в Европе, что вносит свой вклад в разницу в экономию.

На диаграмме ниже показаны 10 стран, в которых наблюдается наибольшая экономия средств при использовании электрического грузового автомобиля:

"Водители по всей Европе уже экономят, переходя на электрические грузовики. Переход на зарядку электромобилей - это будущее отрасли, и SNAP готов помочь водителям и операторам автопарков в этом переходе".

Мэтью Беллами - управляющий директор SNAP.

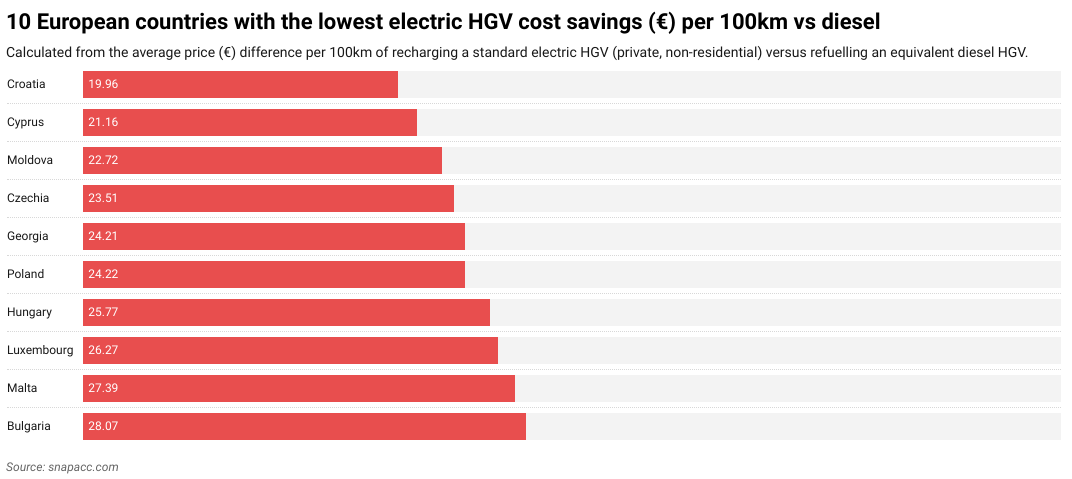

Страны, которые меньше всего экономят, переходя на электрические грузовики

Хорватия (€19,96), Кипр (€21,16) и Молдова (€22,72) - три страны с наименьшей экономией в Европе.

Хорватия занимает второе место в ЕС по темпам внедрения EV (https://www.smf.co.uk/wp-content/uploads/2025/03/Decreasing-transport-poverty-in-Europe-through-public-EV-chargepoints-March2025.pdf) после Польши. Отчасти это связано с неразвитой инфраструктурой зарядки EV в Хорватии, например, зарядными станциями, которые требуют звонка в службу поддержки или использования нескольких различных приложений для запуска процесса зарядки, плохой ориентацией зарядных станций вблизи крупных автомагистралей и потенциально высоким временем ожидания в пик туристического сезона. Кроме того, в Хорватии отсутствуют сверхскоростные зарядные станции (180 кВт и выше), что может стать проблемой для грузовых электромобилей, которым требуется больше энергии, чем обычным EV.

И на Кипре, и в Молдове существуют внутренние геополитические проблемы, которые затрудняют планирование инфраструктуры для зарядки EV (как и национальное планирование в целом). На Кипре северная половина острова, включая половину его столицы Никосии, с 1974 года оккупирована поддерживаемой Турцией Турецкой Республикой Северного Кипра. Для Молдовы восточная провинция Приднестровья действует как государство де-факто с собственным правительством. Это означает, что обе страны не могут последовательно внедрить инфраструктуру EV на территории, которую они считают своей.

Проблемы Кипра также усугубляются высокими ценами на электроэнергию, в то время как в Молдове цены на дизельное топливо пятые по дешевизне в Европе. Молдова также является [второй беднейшей страной Европы] (https://worldpopulationreview.com/country-rankings/poorest-countries-in-europe), что затрудняет инвестиции в инфраструктуру EV. Все эти факторы способствуют общей низкой экономии затрат для электрических грузовых автомобилей.

Польша также занимает низкое место в списке с экономией 24,22 евро. Несмотря на впечатляющий экономический рост и растущие инвестиции в инфраструктуру зарядки EV, ее большие размеры означают, что в некоторых районах страны покрытие все еще остается проблемой, хотя в будущем это, вероятно, [изменится] (https://alternative-fuels-observatory.ec.europa.eu/general-information/news/poland-launches-major-funding-programs-zero-emission-transport).

Такие страны, как Испания (€32,20), Румыния (€30,62) и Ирландия (€30,54), занимают среднюю позицию по экономии затрат на электрические грузовики. Вероятно, это объясняется тем, что в этих странах развита инфраструктура зарядки электромобилей, а стоимость электроэнергии и дизельного топлива находится на среднем уровне.

На диаграмме ниже показаны 10 стран, в которых экономия средств при использовании электрического грузового автомобиля самая низкая:

Экономия затрат на электрический грузовой автомобиль в Великобритании

В Великобритании экономия затрат на электромобили составляет 36,23 евро, что ставит ее на 11-е место по экономии затрат от подзарядки на 100 км. Это во многом объясняется дороговизной топлива в Великобритании, где * цены на дизельное топливо являются третьими по дороговизне в Европе*. Хотя экономия за счет высоких цен на дизельное топливо, безусловно, способствует высокой экономии расходов на электромобили в Великобритании, она могла бы быть гораздо выше, если бы электричество в Великобритании также не было одним из самых дорогих в Европе.

Великобритания также ожидает улучшения инфраструктуры зарядки EV. Британская компания Moto, обслуживающая автострады, активно планирует построить [15 "суперхабов" к 2027 году] (https://www.fleetnews.co.uk/news/electric-hgv-charging-superhubs-planned-for-motorway-services). Эти суперхабы смогут обеспечить более эффективную зарядку EV для eHGV по сравнению со стандартными зарядными устройствами. В настоящее время на дорогах Великобритании имеется менее пяти специальных пунктов зарядки для eHGV. Учитывая, что другие компании, такие как BP Pulse и Aegis Energy, также собираются инвестировать, можно предположить, что в ближайшем будущем в Великобритании появится гораздо более совершенная сеть зарядки грузовых автомобилей.

Что влияет на электрификацию грузовых автомобилей?

В настоящее время на электрификацию грузовых автомобилей влияет несколько факторов, в том числе отсутствие зарядной инфраструктуры, длительное время зарядки, высокие первоначальные затраты на переоборудование грузовиков и их ограниченный запас хода. Кроме того, сравнительно низкая стоимость и доступность дизельного топлива и транспортных средств делают традиционные грузовые автомобили привлекательным вариантом для [операторов автопарков] (https://snapacc.com/fleet-operators/).

Однако все эти последствия могут варьироваться в зависимости от страны эксплуатации. Например, если ваш автопарк работает только внутри страны, такой как Норвегия или Исландия, то он, скорее всего, пострадает меньше, чем автопарк, работающий по всей Европе или в регионах с более слабой инфраструктурой eHGV, например, на Балканах.

Недостаточная зарядная инфраструктура

Основным препятствием на пути электрификации грузовых автомобилей является недостаточная инфраструктура для зарядки электромобилей. Это связано с тем, что для электронных грузовиков требуется мегаваттная зарядка, которую не поддерживает большинство существующих пунктов зарядки EV для пассажирских автомобилей (стандартных электромобилей и фургонов).

В Европе есть много стран, где остро не хватает подобной инфраструктуры, особенно на основных грузовых маршрутах и на стоянках грузовиков. Как правило, это более бедные государства южной и восточной Европы, такие как Молдова, Грузия и Болгария. Неслучайно эти страны входят в первую десятку стран по экономии средств на eHGV.

Бывает и так, что зарядные станции для eHGV существуют, но они находятся в районах, которые просто не могут вместить несколько eHGV, заряжающихся за ночь, из-за слабой местной электросети. Такая проблема часто возникает в сельских и отдаленных районах Европы.

Несмотря на то, что многие европейские страны планируют улучшить инфраструктуру eHGV, это все еще трудоемкий и дорогостоящий процесс, требующий преодоления многочисленных бюрократических, логистических и технических препятствий, не говоря уже о модернизации сопутствующей инфраструктуры, такой как подключение к местным сетям, которая также будет необходима.

Длительное время зарядки

Электрические грузовики заряжаются гораздо дольше, чем стандартные EV. Это означает, что зарядку часто приходится проводить в течение ночи. Даже если удастся приобрести быстрые зарядные устройства для электромобилей, процесс все равно займет [не менее двух часов] (https://dhl-freight-connections.com/en/solutions/charging-times-for-electric-trucks-the-goal-is-less-than-30-minutes/), а не несколько минут, как в случае с бензиновыми автомобилями.

Длительное время зарядки может повлиять на операторов автопарков с точки зрения времени оборота. В отрасли с жесткими графиками и сроками поставок это может потенциально негативно сказаться на эффективности бизнеса.

Ограниченный запас хода электромобилей

Запас хода электрических грузовиков также ограничен по сравнению с пробегом традиционных грузовиков. По данным Safety Shield, запас хода типичного электрического грузовика на одной зарядке составляет около 300 миль (примерно расстояние от Лондона до Роттердама). Однако типичный грузовик с дизельным двигателем может проехать на одном баке топлива до 1 000 миль (примерно расстояние от Лондона до Варшавы).

На пробег электрических грузовиков также могут сильнее влиять внешние факторы, такие как нагрузка, [холодная погода] (https://snapacc.com/newsroom/a-truck-drivers-guide-to-winter-in-europe/) и рельеф местности. Это может привести к беспокойству водителей о дальности пробега, которые могут чаще проводить зарядку, чтобы убедиться, что энергии достаточно для достижения пункта назначения. Это, в свою очередь, может привести к задержкам в доставке, особенно при движении через страны с плохо развитой инфраструктурой зарядки eHGV.

Все это делает [оптимизацию маршрута] (https://snapacc.com/newsroom/route-optimisation-with-fleet-management-software-snap-account/) жизненно важной для операторов автопарков, планирующих поездки для своих eHGV. Следует отметить, что технология аккумуляторных батарей постоянно развивается, и в ближайшем будущем их емкость, а значит, и пробег, будут продолжать увеличиваться.

Высокая стоимость электронного грузовика

Первоначальная стоимость электронного грузовика высока (обычно в пределах £160 000-£200 000, по сравнению с £80 000-£100 000 для дизельного грузовика), что может отпугнуть независимых водителей и небольших операторов автопарков от его приобретения. В основном это связано с дороговизной аккумуляторной технологии. Это означает, что приобретение нового электрического грузовика обойдется недешево, поскольку технология, используемая в нем, дороже, чем в дизельном грузовике.

Высокие первоначальные затраты на покупку электромобилей также означают, что операторы автопарков в странах с более дешевыми тарифами на электроэнергию для зарядки электромобилей, таких как Норвегия, Швеция или Финляндия, с большей вероятностью перейдут на новые технологии, поскольку они быстрее окупят свои инвестиции, чем операторы в странах с дорогой электроэнергией, таких как Ирландия и Хорватия.

Цены на электроэнергию также могут колебаться в зависимости от различных событий. Например, за последние пять лет цены на электроэнергию колебались в связи с открытием экономик после пандемии COVID-19 и вторжением России в Украину в 2022 году (последнее, в частности, оказало значительное влияние на энергоснабжение Европы). В результате в период после вторжения произошел скачок цен на электроэнергию почти на 30 %, с 20,5 до 26,5 евро/кВт-ч для средней столицы ЕС. Однако сейчас средний показатель по ЕС ниже, чем в 2022 году, и, судя по всему, электрозарядка для грузовых автомобилей продолжит свое восхождение.

В Европе средняя стоимость пробега электрического грузовика на 100 км составляет 20,51 евро, что значительно дешевле, чем 51,10 евро для дизельного грузовика на то же расстояние.

По мере повышения эффективности и распространения аккумуляторных технологий, а также снижения стоимости производства, автомобили eHGV будут становиться все более доступными для приобретения.

Дешевизна и доступность дизельного топлива

Дизельное топливо по-прежнему играет доминирующую роль в индустрии грузовых автомобилей. Это объясняется тем, что инфраструктура для дизельного топлива была хорошо развита в Европе на протяжении десятилетий, особенно по сравнению с электрическими зарядными устройствами для грузовых автомобилей. Совместимость дизельного топлива с [топливными картами] (https://snapacc.com/newsroom/fuel-cards-in-transportation-how-snap-simplifies-fleet-life/) и его относительная дешевизна также сохраняют его популярность среди менеджеров грузовых автопарков.

Однако, как и в случае с электричеством, стоимость дизельного топлива колеблется по всему континенту. Поэтому в таких странах, как Молдова, Грузия и Мальта, где дизельное топливо остается дешевым, выгоднее использовать дизельные грузовики. И наоборот, в таких странах, как Исландия и Нидерланды, где дизельное топливо относительно дорого, есть больше стимулов для перехода на электрические грузовики.

Страны с дешевым топливом также могут не решиться вкладывать значительные средства в инфраструктуру электронного грузового транспорта, опасаясь оттолкнуть от себя традиционные автопарки грузовиков, которые в результате могут выбрать альтернативные маршруты.

Будущее электрических грузовиков в Европе

Электрические грузовики - это долгосрочное будущее автоперевозок. Они не только дешевле в эксплуатации с течением времени, но и благодаря тому, что в новую инфраструктуру инвестируют и строят ее высокими темпами, они также станут гораздо более жизнеспособными с финансовой и стратегической точек зрения.

Помимо экономических преимуществ, электрические грузовые автомобили также важны с точки зрения их вклада в достижение экологических целей, таких как Net Zero. Поскольку традиционные грузовые автомобили являются крупными загрязнителями окружающей среды, сэкономленные выбросы от использования электромобилей будут ощущаться в более чистом воздухе по всей Европе.

Следующие тенденции (https://snapacc.com/newsroom/the-road-ahead-for-2025-truck-industry-trends-to-expect/) могут повлиять на электрические грузовые автомобили в будущем:

- Smart truck parks: Truck parks in the future will evolve to better accommodate eHGVs alongside other smart technological advancements. These truck parks may include up-to-date ultra-fast charging stations, diagnostic machines, battery swap stations, and automated cleaning services, among other features.

- Increased EU regulations: Low Emission Zones (LEZs) already exist in a number of cities (e.g. Paris, Berlin, and Milan) with more European cities likely to follow suit with more stringent EU transport regulations. Fleet operators may opt for eHGVs to meet EU regulations or retrofit their HGVs with cleaner technologies, like smart tachographs.

- AI implementation: AI technology has already had a profound sustainability impact across road haulage — with applications in route optimisation, predictive maintenance, and autonomous vehicle development. Electric vehicles will likely incorporate AI to help drive sustainability in the haulage industry over the coming decades.

- Sustainability: The shift to eHGVs is part of a wider global push toward sustainable living. The effects of extreme weather, including heatwaves and floods across Europe, show no sign of slowing due to climate change. Moving to electric HGVs is one way the world is reducing its dependence on fossil fuels.

- Fuel variety: During the transition to cleaner fuel sources, there will be a variety of HGV types on the road throughout the 2030s. Many will be older diesel models, some will be electric, and others will be powered by alternative fuels such as biofuel made from renewable biomass sources.

Управляйте расходами на электрогрузовики более разумно

Электрические грузовые автомобили - это будущее, и в этом мало кто сомневается. Экономические и экологические преимущества приведут к тому, что в ближайшие годы все больше операторов автопарков и водителей перейдут на электромобили. Как долго продлится этот переходный период, будет зависеть от того, насколько быстро Европа сможет развить инфраструктуру для зарядки электромобилей.

В настоящее время на континенте есть значительные участки, на которых электронные грузовики неэффективны и требуют значительной оптимизации маршрута из-за меньшего радиуса действия. Кроме того, первоначальные затраты могут отпугнуть независимых водителей и небольших операторов автопарков.

Технологии и инфраструктура будут совершенствоваться, и уже сейчас существуют сервисы, призванные максимально упростить управление парком электронных грузовиков и связанные с этим расходы. От оптимизации маршрутов и управления автопарком до карт парковок и моек для грузовиков - SNAP делает грузоперевозки простыми.

[Подпишитесь на SNAP сегодня.] (https://snapacc.com/sign-up/)