Guest

Carburante vs carica: Il passaggio all'elettrico è più economico o semplicemente più verde?

Creato: 28/07/2025

•

Aggiornato: 19/09/2025

La crescita delle stazioni di ricarica elettrica per i mezzi pesanti in Europa ha portato a un periodo di transizione sulle vaste reti stradali del continente. Per molti operatori di flotte e conducenti, i classici mezzi pesanti alimentati a diesel sono ancora la scelta di trasporto. Tuttavia, il passaggio ai mezzi pesanti elettrici è imminente, in quanto il settore continua a evolversi.

Per valutare la fattibilità del passaggio dal diesel all'elettrico da parte di operatori di flotta, SNAP ha condotto una ricerca sui costi di ricarica dei mezzi pesanti rispetto al rifornimento di carburante su diverse rotte di trasporto merci europee. Abbiamo calcolato il risparmio di elettricità rispetto al diesel in euro per 100 km in 35 Paesi europei.

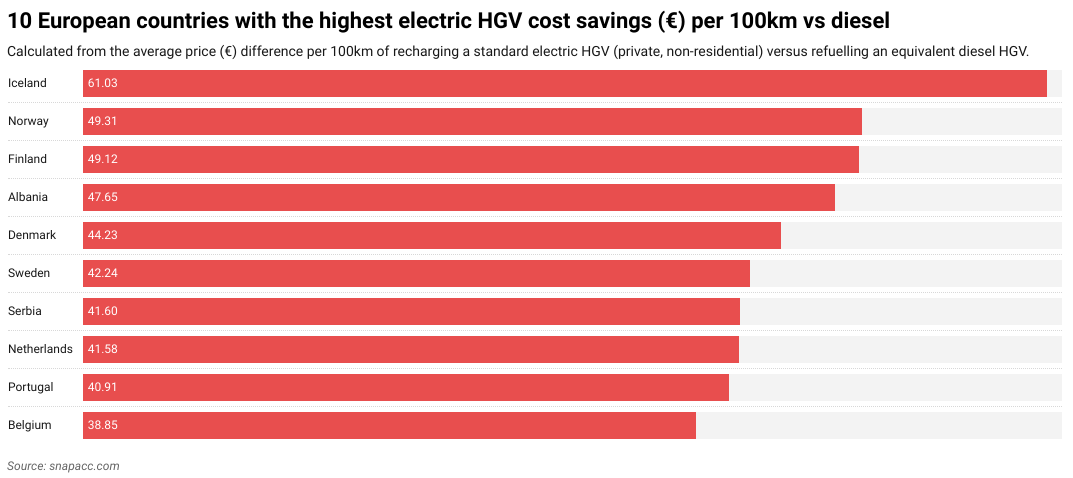

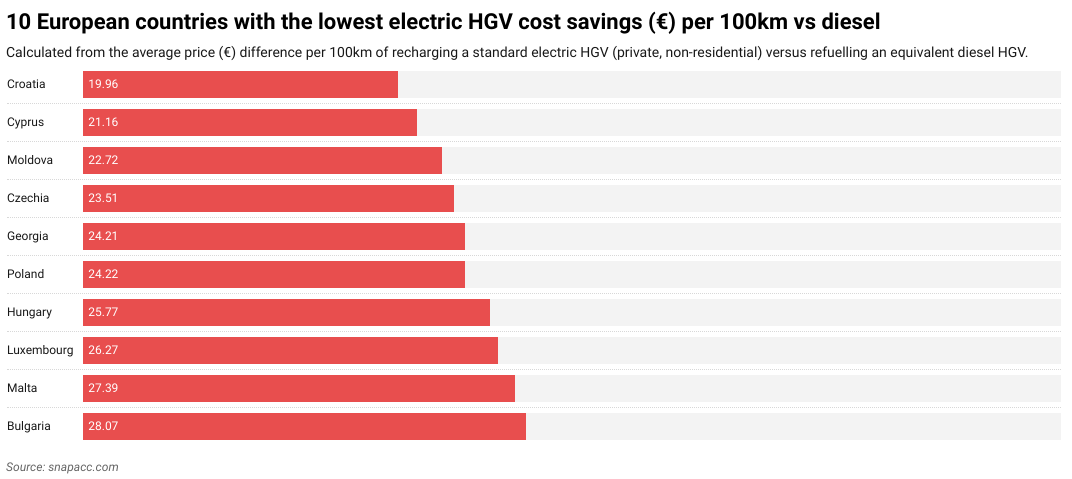

Abbiamo riscontrato che l'Islanda è in testa con un risparmio medio di 61,03 euro per 100 km, mentre i paesi nordici Norvegia e Finlandia offrono rispettivamente il secondo e il terzo risparmio più elevato. All'altra estremità della scala, la Croazia ha offerto il minor numero di risparmi sui costi con 19,96 euro per 100 km, seguita da Cipro e dalla Moldavia.

In questo articolo, scopriamo i risparmi sui costi per paese europeo e analizziamo alcuni dei risparmi sui costi per paese europeo e analizziamo alcuni dei fattori esterni che possono influenzare questi risparmi. Ci addentriamo anche in quello che potrebbe essere il futuro degli eHGV in Europa e in che modo gli eHGV possono aiutare gli operatori delle flotte e i conducenti a risparmiare, in particolare con i driver budgets.

Come i costi dell'eHGV e del gasolio si confrontano nell'UE

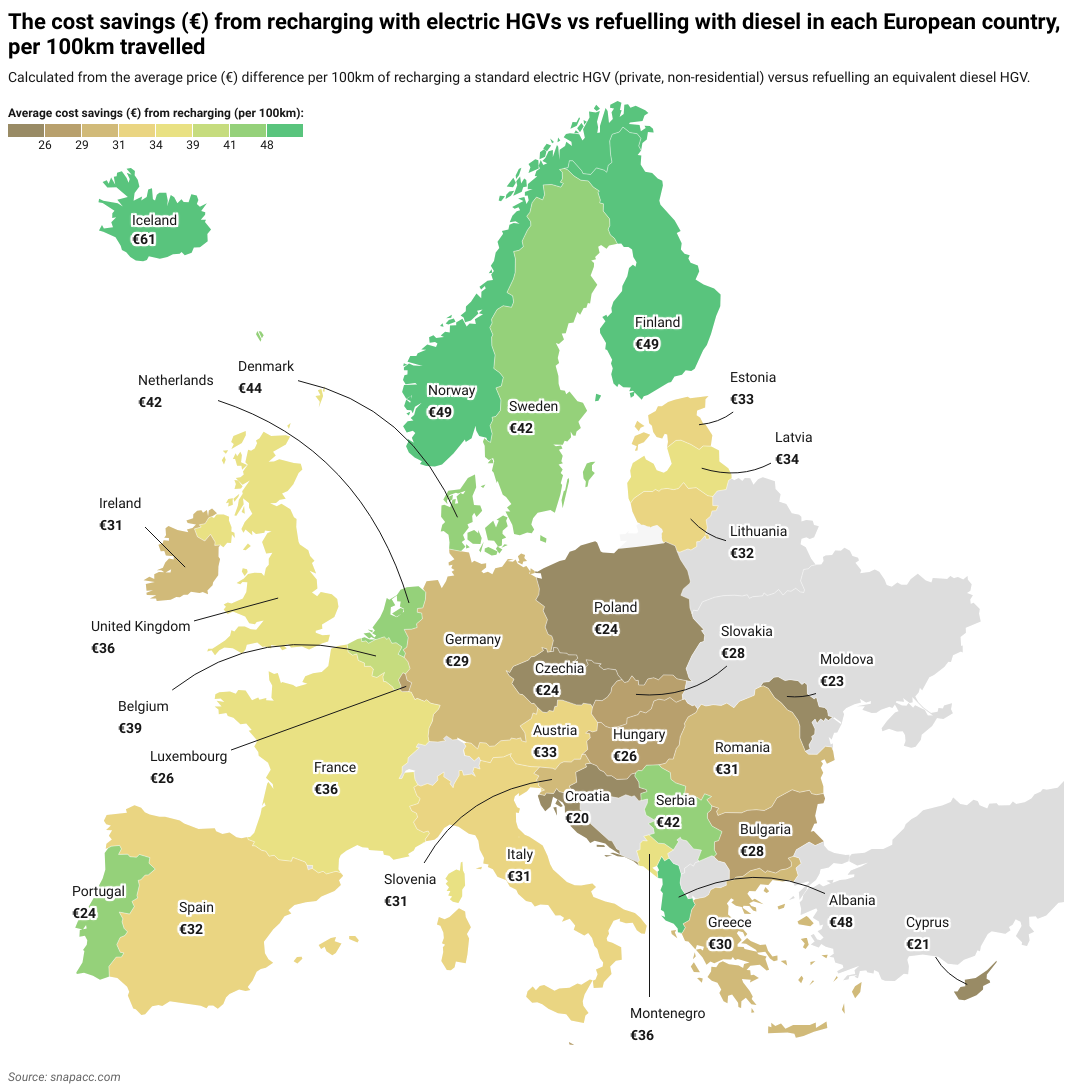

Dalla nostra ricerca è emerso che, in tutti i Paesi europei esaminati, l'utilizzo di un veicolo elettrico con ricarica elettrica ha permesso di risparmiare rispetto a un veicolo pesante tradizionale con carburante. La differenza principale è stata l'entità dei risparmi. Ad esempio, il prezzo dell'elettricità nel paese più costoso, l'Islanda, è superiore del 206%** (41 euro in più) rispetto al paese meno costoso, la Croazia.

Abbiamo riscontrato che, in media, un autista di un mezzo pesante elettrico risparmierà 30,59 euro per 100 km rispetto a un autista di un mezzo pesante diesel. Ciò si traduce in un risparmio medio stimato di 37.200 euro* all'anno per i conducenti di mezzi pesanti elettrici a lungo raggio e di 24.800 euro per i conducenti nazionali*.

Per compilare i nostri dati, abbiamo preso in considerazione 35 Paesi europei e abbiamo confrontato il costo dell'energia o del carburante per 100 km per due tipi di veicoli commerciali pesanti (HGV). Si trattava di un mezzo pesante diesel standard, ipotizzando un consumo di carburante di 35 litri per 100 km al prezzo medio al dettaglio del gasolio in ciascun Paese, e di un mezzo pesante elettrico, ipotizzando un consumo di elettricità di 108 kWh per 100 km basato sulla tariffa media dell'elettricità non domestica. L'IVA e le imposte recuperabili sono state escluse da questi calcoli. Il confronto riflette solo i costi diretti "alla pompa" o "alla spina", senza tenere conto di fattori quali le dimensioni della flotta, i contratti energetici negoziati o le future variazioni dei prezzi di carburante ed elettricità.

Per la ricerca dei prezzi del gasolio e dell'elettricità sono state utilizzate diverse fonti, tra cui Eurostat, CEIC, GlobalPetrolPrices, Webfleet e Gov.uk. Vale la pena notare che alcune di queste fonti si riferiscono alla "Gran Bretagna" mentre altre al "Regno Unito". Ai fini della presente ricerca, i due termini sono stati trattati in modo intercambiabile.

Paesi che risparmiano di più con la conversione ai mezzi pesanti elettrici

Islanda (61,03 euro), Norvegia (49,31 euro) e Finlandia (49,12 euro) sono attualmente i Paesi in cui si può risparmiare di più convertendosi a un veicolo pesante elettrico.

Ciò è dovuto in gran parte al fatto che questi Paesi sono tra i più cari in Europa per il gasolio. L'Islanda è il Paese più caro d'Europa per il gasolio (2,07 euro al litro). Questo costo elevato deriva in gran parte dal suo isolamento geografico rispetto al resto d'Europa, che rende il costo dell'importazione di gasolio molto più alto rispetto a quello di altri Paesi europei. L'Islanda, come la Norvegia e la Finlandia, è nota anche per l'elevata aliquota fiscale, che contribuisce anch'essa al costo elevato del carburante.

La Norvegia (32%) e l'Islanda (18%) sono anche i primi due Paesi al mondo per quanto riguarda le auto elettriche in circolazione come percentuale di autovetture circolanti. Di conseguenza, entrambi i Paesi hanno investito in modo significativo nelle infrastrutture di ricarica elettrica.

Le dimensioni ridotte e la tangenziale principale dell'Islanda facilitano inoltre l'installazione di stazioni di ricarica elettrica a intervalli regolari per i conducenti di mezzi pesanti elettrici. Lo stesso ragionamento può essere in parte utilizzato per altri Paesi con reti più piccole che hanno un alto tasso di risparmio sui costi, tra cui l'Albania, la Serbia e il Belgio - anche se va notato che tutti e tre hanno anche alcuni dei prezzi del gasolio più cari d'Europa, il che contribuisce alla differenza di risparmio sui costi.

Il grafico seguente mostra i 10 Paesi che registrano i maggiori risparmi sui costi di utilizzo di un camion elettrico:

Gli autisti di tutta Europa stanno già risparmiando passando ai mezzi pesanti elettrici. Il passaggio alla ricarica degli eHGV è il futuro del settore e SNAP è pronta ad aiutare i conducenti e gli operatori di flotte nella transizione ".

Matthew Bellamy - Direttore generale di SNAP

I Paesi che risparmiano di meno con la conversione ai mezzi pesanti elettrici

Croazia (19,96 euro), Cipro (21,16 euro) e Moldavia (22,72 euro) sono attualmente i tre Paesi con i minori risparmi in Europa.

La Croazia ha il [secondo più lento tasso di adozione dei veicoli elettrici] (https://www.smf.co.uk/wp-content/uploads/2025/03/Decreasing-transport-poverty-in-Europe-through-public-EV-chargepoints-March2025.pdf) nell'UE dopo la Polonia. Ciò è dovuto in parte alle scarse infrastrutture di ricarica dei veicoli elettrici in Croazia, come le stazioni di ricarica che richiedono uno squillo al servizio clienti o l'utilizzo di diverse applicazioni per avviare il processo di ricarica, le scarse indicazioni per le stazioni di ricarica al di fuori delle principali autostrade e i tempi di attesa potenzialmente elevati durante l'alta stagione turistica. Inoltre, la Croazia non dispone di stazioni di ricarica ad altissima velocità (180 kW e oltre), che (180 kW e oltre), il che può rappresentare un problema per i mezzi pesanti elettrici che richiedono una potenza maggiore rispetto alla media dei veicoli elettrici.

Sia Cipro che la Moldavia hanno problemi geopolitici interni che rendono difficile la pianificazione delle infrastrutture per la ricarica dei veicoli elettrici (così come la pianificazione nazionale in generale). Per quanto riguarda Cipro, la metà settentrionale dell'isola - compresa la metà della sua capitale, Nicosia - è [occupata dalla Repubblica turca di Cipro del Nord] (https://www.bbc.co.uk/news/world-europe-17217956) dal 1974. Per la Moldavia, la provincia orientale della Transnistria agisce come uno Stato de facto con un proprio governo. Ciò significa che entrambi i Paesi non sono in grado di implementare infrastrutture EV in modo coerente nel territorio che considerano proprio.

I problemi di Cipro sono aggravati anche dagli alti costi dell'elettricità, mentre la Moldavia ha il quinto prezzo del gasolio più basso d'Europa. La Moldavia è anche il [secondo Paese più povero d'Europa] (https://worldpopulationreview.com/country-rankings/poorest-countries-in-europe), il che rende difficile l'investimento in infrastrutture per veicoli elettrici. Tutti questi fattori contribuiscono a un risparmio complessivo dei costi per i mezzi pesanti elettrici.

Anche la Polonia è in fondo alla lista, con un risparmio di 24,22€. Nonostante l'impressionante crescita economica e i crescenti investimenti nelle infrastrutture di ricarica dei veicoli elettrici, le sue grandi dimensioni fanno sì che la copertura sia ancora un problema in alcune aree del Paese, anche se questo sembra destinato a [cambiare in futuro] (https://alternative-fuels-observatory.ec.europa.eu/general-information/news/poland-launches-major-funding-programs-zero-emission-transport).

Paesi come la Spagna (32,20 euro), la Romania (30,62 euro) e l'Irlanda (30,54 euro) occupano la posizione intermedia per quanto riguarda il risparmio sui costi dei mezzi pesanti elettrici. Ciò è probabilmente dovuto al fatto che questi Paesi dispongono di una crescente infrastruttura di ricarica per i veicoli elettrici e di costi medi per l'elettricità e il gasolio.

Il grafico seguente mostra i 10 Paesi che registrano i minori risparmi sui costi di utilizzo dei mezzi pesanti elettrici:

Risparmio sui costi dei mezzi pesanti elettrici nel Regno Unito

Il Regno Unito ha un risparmio sui costi degli eHGV di 36,23 euro, che lo colloca all'undicesimo posto assoluto per quanto riguarda il risparmio sui costi di ricarica per 100 km. Ciò è dovuto in gran parte al costo del carburante nel Regno Unito, con i prezzi del diesel che sono i terzi più cari in Europa. Sebbene il risparmio derivante dagli alti costi del diesel contribuisca certamente all'elevato risparmio sui costi degli eHGV nel Regno Unito, esso sarebbe probabilmente molto più elevato se l'elettricità nel Regno Unito non fosse anche tra le più costose in Europa.

Anche nel Regno Unito sono previsti miglioramenti all'infrastruttura di ricarica dei veicoli elettrici. La società di servizi autostradali britannica Moto sta pianificando attivamente la costruzione di 15 "superhub" entro il 2027. Questi superhub possono ospitare la ricarica dei veicoli elettrici in modo più efficiente rispetto ai caricabatterie standard. Attualmente ci sono meno di cinque punti di ricarica dedicati agli eHGV sulle strade del Regno Unito. Con altre aziende come BP Pulse e Aegis Energy che intendono investire, sembra probabile che il Regno Unito avrà una rete di ricarica per mezzi pesanti molto migliorata nel prossimo futuro.

Cosa ostacola l'elettrificazione dei mezzi pesanti?

L'elettrificazione dei mezzi pesanti è attualmente ostacolata da diversi fattori, tra cui la mancanza di infrastrutture di ricarica, i lunghi tempi di ricarica, gli elevati costi iniziali di conversione dei mezzi pesanti e la loro autonomia limitata. Inoltre, il costo relativamente basso e l'accessibilità del carburante e dei veicoli diesel rendono i mezzi pesanti tradizionali un'opzione attraente per gli operatori delle flotte.

Tuttavia, tutti questi impatti possono variare a seconda del Paese in cui si opera. Ad esempio, se la vostra flotta opera solo a livello nazionale in un paese come la Norvegia o l'Islanda, è probabile che sia meno colpita di una flotta che opera in tutta Europa o in regioni con infrastrutture eHGV più carenti, come i Balcani.

Infrastruttura di ricarica insufficiente

Il principale ostacolo all'elettrificazione dei mezzi pesanti è l'insufficienza delle infrastrutture di ricarica per i veicoli elettrici pesanti. Questo perché gli eHGV richiedono una ricarica su scala megawatt, che la maggior parte dei punti di ricarica EV esistenti per i veicoli passeggeri (auto e furgoni elettrici standard) non supporta.

Ci sono molti Paesi in Europa che mancano gravemente di queste infrastrutture, soprattutto sulle principali vie di trasporto e negli autogrill. Si tratta tendenzialmente degli Stati più poveri dell'Europa meridionale e orientale, come la Moldavia, la Georgia e la Bulgaria. Non è una coincidenza che questi Paesi si collochino agli ultimi 10 posti per quanto riguarda i risparmi sui costi dei veicoli elettrici pesanti.

Può anche accadere che le stazioni di ricarica per eHGV esistano, ma si trovino in aree che semplicemente non possono ospitare più eHGV in carica durante la notte a causa della debolezza della rete elettrica locale. Questo è spesso un problema nelle zone più rurali e remote d'Europa.

Sebbene molti Paesi europei stiano pianificando il miglioramento dell'infrastruttura eHGV, si tratta ancora di un processo lungo e costoso, con numerosi ostacoli burocratici, logistici e tecnici da superare - per non parlare degli aggiornamenti delle infrastrutture circostanti, come i collegamenti alla rete locale, che saranno necessari.

Tempi di ricarica lunghi

La ricarica dei mezzi pesanti elettrici è molto più lunga di quella dei veicoli elettrici standard. Ciò significa che spesso la ricarica deve avvenire durante la notte. Anche se è possibile acquistare caricatori rapidi per i veicoli elettrici, il processo richiede comunque almeno due ore, anziché pochi minuti, come nel caso dei veicoli a benzina.

Questo lungo tempo di ricarica può avere un effetto a catena per gli operatori delle flotte in termini di tempi di rotazione. In un settore in cui i tempi di consegna e le scadenze sono stretti, ciò può essere potenzialmente dannoso per le prestazioni aziendali.

Autonomia limitata dei veicoli commerciali leggeri

I mezzi pesanti elettrici sono anche limitati dalla loro autonomia relativamente limitata rispetto al chilometraggio offerto dai mezzi pesanti tradizionali. Secondo Safety Shield, un tipico veicolo commerciale elettrico ha un'autonomia di circa 300 miglia con una singola carica (all'incirca la distanza da Londra a Rotterdam). Un tipico veicolo commerciale diesel, invece, può percorrere fino a 1.000 miglia con un solo pieno di carburante (all'incirca la distanza da Londra a Varsavia).

Il chilometraggio dei mezzi pesanti elettrici può anche essere maggiormente influenzato da fattori esterni come il carico, il [clima freddo] (https://snapacc.com/newsroom/a-truck-drivers-guide-to-winter-in-europe/) e il terreno. Ciò può causare ansia da autonomia per i conducenti, che possono effettuare ricariche più frequenti per assicurarsi di avere energia sufficiente per raggiungere la destinazione. Questo, a sua volta, può portare a ritardi nelle consegne, soprattutto quando si attraversano paesi con scarse infrastrutture di ricarica per eHGV.

Tutto ciò rende l'ottimizzazione del percorso vitale per gli operatori delle flotte che pianificano i viaggi dei loro eHGV. Va notato che la tecnologia delle batterie è in continua evoluzione e la capacità - e quindi il chilometraggio - continuerà a migliorare nel prossimo futuro.

Costi elevati degli eHGV

Il costo iniziale di un eHGV è elevato (tipicamente tra £160.000-£200.000, rispetto a £80.000-£100.000 per un HGV diesel) e ciò può potenzialmente scoraggiare i conducenti indipendenti e i piccoli operatori di flotte dal possederne uno. Ciò è dovuto in gran parte al costo della tecnologia delle batterie. Ciò significa che sarà costoso acquistare un nuovo veicolo commerciale elettrico a titolo definitivo, poiché la tecnologia al suo interno è più costosa di quella di un veicolo commerciale diesel.

Gli elevati costi iniziali di acquisto dei veicoli elettrici leggeri fanno sì che i gestori di flotte in paesi con tariffe elettriche più convenienti per la ricarica dei veicoli elettrici leggeri, come la Norvegia, la Svezia o la Finlandia, siano più propensi a convertirsi, in quanto recupereranno più rapidamente l'investimento rispetto a quelli in paesi con elettricità costosa, come l'Irlanda e la Croazia.

I prezzi dell'elettricità possono fluttuare anche in relazione a vari eventi. Ad esempio, negli ultimi cinque anni, i prezzi dell'elettricità hanno fluttuato in risposta all'apertura delle economie dopo la pandemia COVID-19 e all'invasione dell'Ucraina da parte della Russia nel 2022 (quest'ultima, in particolare, ha avuto effetti importanti sull'approvvigionamento energetico europeo). Di conseguenza, nel periodo successivo all'invasione, i prezzi dell'elettricità hanno subito un'impennata di quasi il 30%, passando da 20,5 c€/kWh a 26,5 c€/kWh per la capitale media dell'UE. Con la media dell'UE ora, tuttavia, inferiore a quella del 2022, sembra che la ricarica elettrica per i mezzi pesanti sia destinata a continuare la sua ascesa.

In tutta Europa, il costo medio di gestione di un camion elettrico per 100 km è di 20,51 euro, molto più basso rispetto ai 51,10 euro di un camion diesel per la stessa distanza.

Con il miglioramento dell'efficienza e con la diffusione della tecnologia delle batterie e la riduzione dei costi di produzione, anche i veicoli elettrici leggeri diventeranno più accessibili.

Economicità e accessibilità del gasolio

Il gasolio gioca ancora un ruolo dominante nel settore dei mezzi pesanti. Questo perché l'infrastruttura del diesel è ben consolidata in Europa da decenni, soprattutto rispetto ai caricabatterie elettrici per i mezzi pesanti. La compatibilità del diesel con le [carte carburante] (https://snapacc.com/newsroom/fuel-cards-in-transportation-how-snap-simplifies-fleet-life/) e la sua relativa economicità lo rendono popolare tra i gestori di flotte di camion.

Come per l'elettricità, tuttavia, il valore del gasolio fluttua in tutto il continente. Per questo motivo, in paesi come la Moldavia, la Georgia e Malta, dove il gasolio rimane a buon mercato, può risultare più vantaggioso mantenere i mezzi pesanti diesel. Al contrario, in nazioni come l'Islanda e i Paesi Bassi, dove il diesel è relativamente costoso, è maggiore l'incentivo a passare a un camion elettrico.

Un Paese con un carburante a basso costo può anche essere più esitante a investire pesantemente nell'infrastruttura eHGV per paura di allontanare le flotte di mezzi pesanti tradizionali, che potrebbero di conseguenza scegliere percorsi alternativi.

Il futuro dei mezzi pesanti elettrici in Europa

I mezzi pesanti elettrici sono il futuro a lungo termine del trasporto su strada. Non solo sono più economici da gestire nel tempo, ma con le nuove infrastrutture che vengono investite e costruite ad un ritmo sostenuto, diventeranno anche molto più redditizi dal punto di vista finanziario e strategico.

Oltre ai vantaggi economici, i mezzi pesanti elettrici sono importanti anche per il loro contributo agli obiettivi ambientali come Net Zero. Poiché i mezzi pesanti tradizionali sono inquinanti su larga scala, le emissioni risparmiate dai veicoli elettrici si tradurranno in un'aria più pulita in tutta Europa.

Le seguenti tendenze sembrano destinate ad avere un impatto sui mezzi pesanti elettrici in futuro:

- Smart truck parks: Truck parks in the future will evolve to better accommodate eHGVs alongside other smart technological advancements. These truck parks may include up-to-date ultra-fast charging stations, diagnostic machines, battery swap stations, and automated cleaning services, among other features.

- Increased EU regulations: Low Emission Zones (LEZs) already exist in a number of cities (e.g. Paris, Berlin, and Milan) with more European cities likely to follow suit with more stringent EU transport regulations. Fleet operators may opt for eHGVs to meet EU regulations or retrofit their HGVs with cleaner technologies, like smart tachographs.

- AI implementation: AI technology has already had a profound sustainability impact across road haulage — with applications in route optimisation, predictive maintenance, and autonomous vehicle development. Electric vehicles will likely incorporate AI to help drive sustainability in the haulage industry over the coming decades.

- Sustainability: The shift to eHGVs is part of a wider global push toward sustainable living. The effects of extreme weather, including heatwaves and floods across Europe, show no sign of slowing due to climate change. Moving to electric HGVs is one way the world is reducing its dependence on fossil fuels.

- Fuel variety: During the transition to cleaner fuel sources, there will be a variety of HGV types on the road throughout the 2030s. Many will be older diesel models, some will be electric, and others will be powered by alternative fuels such as biofuel made from renewable biomass sources.

Gestire i costi degli eHGV in modo più intelligente

I mezzi pesanti elettrici sono il futuro, su questo ci sono pochi dubbi. Grazie ai vantaggi economici e ambientali, nei prossimi anni un numero sempre maggiore di operatori di flotte e di conducenti passerà ai mezzi pesanti elettrici. La durata di questo periodo di transizione dipenderà dalla rapidità con cui l'Europa riuscirà a sviluppare l'infrastruttura di ricarica dei veicoli elettrici.

Attualmente vi sono ampie zone del continente in cui gli eHGV non sono redditizi e richiedono un'ampia ottimizzazione dei percorsi a causa della loro ridotta autonomia. Inoltre, i costi iniziali possono scoraggiare gli autisti indipendenti e gli operatori di flotte più piccole.

La tecnologia e l'infrastruttura continueranno a migliorare e ci sono già servizi progettati per semplificare al massimo la gestione delle flotte di eHGV e dei relativi costi. Dall'ottimizzazione dei percorsi alla gestione della flotta, fino alle mappe per il parcheggio e il lavaggio dei camion, SNAP semplifica l'attività di autotrasportatore.