Guest

Паливо vs заряд: Перехід на електромобілі дешевший чи просто екологічніший?

Створено: 28.07.2025

•

Оновлено: 19.09.2025

Зростання кількості електричних зарядних станцій для вантажівок по всій Європі призвело до перехідного періоду на великих дорожніх мережах континенту. Для багатьох операторів автопарків і водіїв класичні вантажівки на дизельному паливі все ще залишаються кращим транспортом. Однак перехід на електричні вантажівки вже намічається, оскільки галузь продовжує розвиватися.

Щоб оцінити доцільність переходу операторів автопарків з дизельного на електричний транспорт, SNAP провів дослідження витрат на підзарядку вантажівок у порівнянні з їх заправкою на різних європейських вантажних маршрутах. Ми розрахували економію електроенергії порівняно з дизельним паливом у євро на 100 км у 35 європейських країнах.

Ми виявили, що Ісландія лідирує з середньою економією витрат у розмірі 61,03 євро на 100 км, а Норвегія та Фінляндія посідають друге та третє місця за рівнем економії витрат відповідно. З іншого боку, Хорватія запропонувала найменшу економію витрат - **19,96 євро на 100 км, за нею йдуть Кіпр і Молдова.

У цій статті ми розкриваємо економію витрат у кожній європейській країні та аналізуємо деякі з них, а також аналізуємо деякі зовнішні фактори, які можуть впливати на цю економію. Ми також заглиблюємося в те, яким може бути майбутнє електромобілів у Європі, а також у те, як електромобілі можуть допомогти операторам автопарків і водіям заощадити гроші, зокрема, на [бюджеті водія] (https://snapacc.com/newsroom/a-truck-drivers-guide-to-budgeting/).

Як співвідносяться витрати на електромобілі та дизельне пальне в ЄС

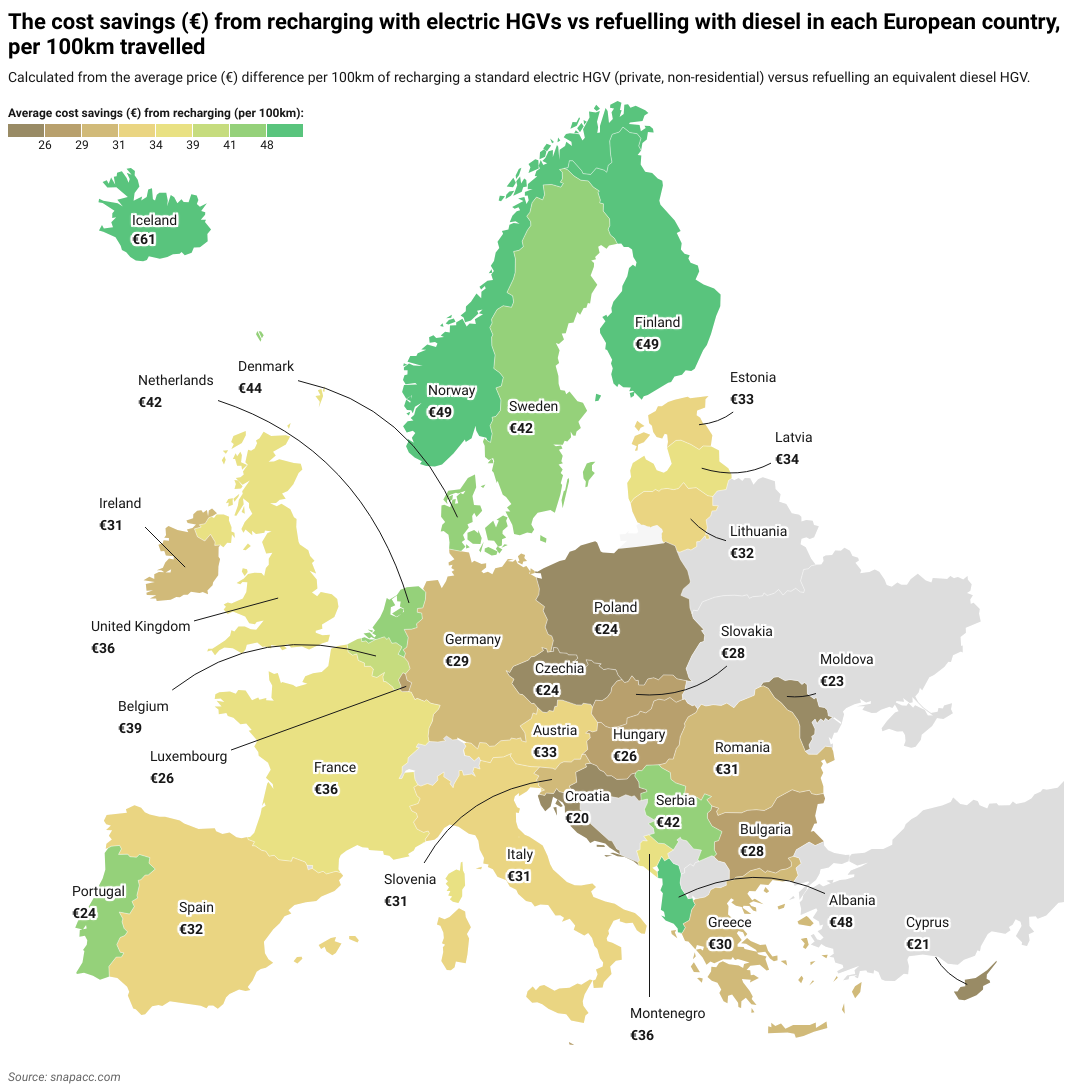

Наше дослідження показало, що в кожній досліджуваній європейській країні використання електромобіля з електричною зарядкою заощаджує кошти порівняно з використанням традиційного вантажного автомобіля на паливі. Основна відмінність полягала в тому, наскільки сильно варіювалася економія витрат. Наприклад, ціна на електроенергію в найдорожчій країні, Ісландії, на 206% вища (на 41 євро), ніж у найдешевшій країні, Хорватії.

Ми виявили, що в середньому водій електричного вантажного автомобіля заощаджує 30,59 євро на 100 км порівняно з водієм дизельного вантажного автомобіля. Це означає, що, за оцінками, середня економія становить 37 200 євро на рік для водіїв електричних вантажівок на далекі відстані та 24 800 євро для водіїв, які здійснюють внутрішні перевезення.

Щоб зібрати наші дані, ми розглянули 35 європейських країн і порівняли витрати енергії або палива на 100 км для двох типів великовантажних транспортних засобів (ВТЗ). Це були стандартні дизельні вантажівки з витратою палива 35 літрів на 100 км за середньою роздрібною ціною на дизельне паливо в кожній країні та електричні вантажівки з витратою електроенергії 108 кВт/год на 100 км за середнім тарифом на електроенергію для непобутових споживачів. ПДВ та податки, що підлягають відшкодуванню, були виключені з цих розрахунків. Порівняння відображає лише прямі витрати "на виході з бензоколонки" або "з розетки", без урахування таких факторів, як розмір автопарку, укладені енергетичні контракти або майбутні зміни цін на паливо та електроенергію.

При дослідженні цін на дизельне паливо та електроенергію було використано низку джерел, зокрема [Eurostat] (https://ec.europa.eu/eurostat/databrowser/view/nrgpc205_custom16953972/default/table?lang=en), [CEIC] (https://www.ceicdata.com/en/iceland/electricity-price-nonhousehold-consumers), [GlobalPetrolPrices] (https://www.globalpetrolprices.com/), [Webfleet] (https://www.webfleet.com/en_gb/webfleet/blog/how-much-diesel-does-a-truck-use-per-mile/) та [Gov.uk] (https://www.gov.uk/government/collections/road-fuel-and-other-petroleum-product-prices). Варто зазначити, що деякі з цих джерел посилаються на "Велику Британію", а інші - на "Сполучене Королівство". Для цілей цього дослідження обидва терміни розглядаються як взаємозамінні.

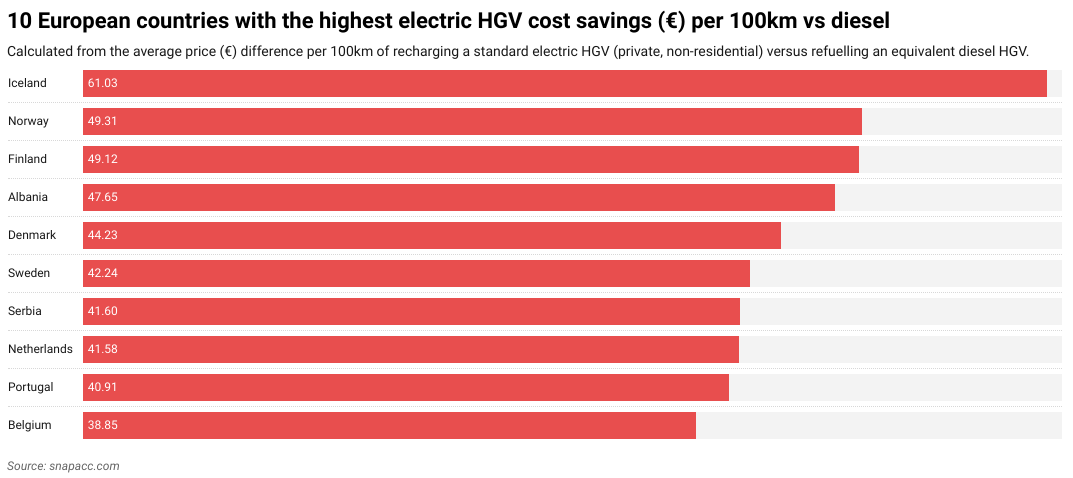

Країни, які заощаджують найбільше за рахунок переходу на електричні вантажівки

Ісландія (61,03 євро), Норвегія (49,31 євро) та Фінляндія (49,12 євро) наразі є країнами, де найбільше можна заощадити, перейшовши на електричні вантажівки.

Це значною мірою пов'язано з тим, що в цих країнах дизельне пальне є одним з найдорожчих в Європі. Ісландія є найдорожчою країною в Європі за ціною на дизельне пальне (2,07 євро за літр). Така висока вартість значною мірою пояснюється її географічною ізоляцією порівняно з рештою Європи, внаслідок чого вартість імпорту дизельного палива значно вища, ніж в інших європейських країнах. Ісландія, як і Норвегія та Фінляндія, також відома своїми високими податковими ставками, що також сприяє високій вартості палива.

Норвегія (32%) та Ісландія (18%) також складають дві провідні країни світу за часткою електромобілів на дорогах від загальної кількості легкових автомобілів на дорогах. Як наслідок, обидві країни інвестували значні кошти в інфраструктуру електрозарядок.

Невеликий розмір Ісландії та наявність головної кільцевої дороги також полегшують встановлення електрозарядних станцій через рівні проміжки часу для водіїв електричних вантажівок. Ці ж міркування можна частково використати для інших країн з меншими мережами, які мають високий рівень економії витрат, зокрема Албанії, Сербії та Бельгії - хоча слід зазначити, що всі три країни мають одні з найдорожчих цін на дизельне паливо в Європі, що також впливає на різницю в економії витрат.

На діаграмі нижче показано 10 країн, які мають найбільшу економію витрат при використанні електричних вантажівок:

*"Водії по всій Європі вже заощаджують, переходячи на електричні вантажівки. Перехід на зарядки для електромобілів - це майбутнє галузі, і SNAP готова допомогти водіям та операторам автопарків у цьому переході".

Метью Белламі - керуючий директор SNAP

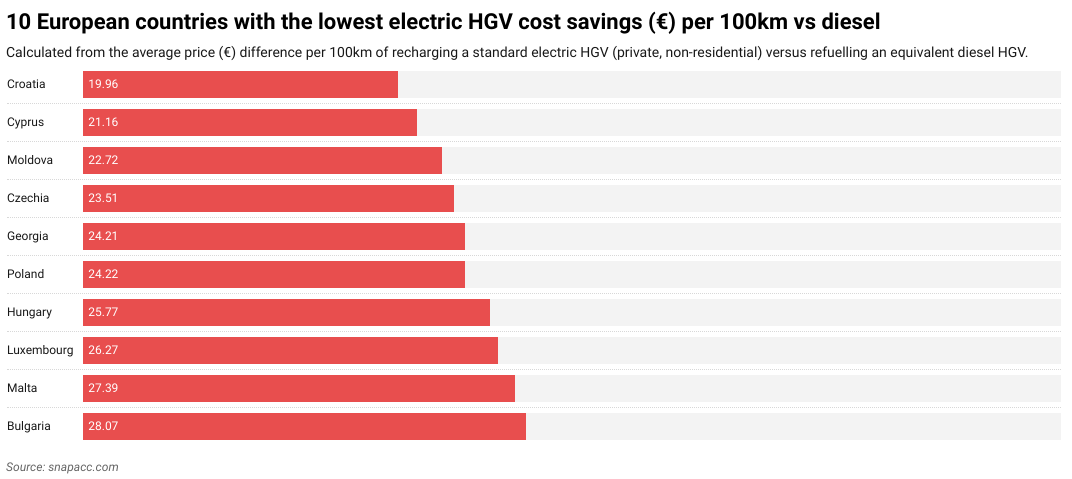

Країни, які заощаджують найменше за рахунок переходу на електричні вантажівки

Хорватія (19,96 євро), Кіпр (21,16 євро) та Молдова (22,72 євро) наразі є трьома країнами з найнижчим рівнем економії в Європі.

Хорватія посідає [друге місце за темпами впровадження електромобілів] (https://www.smf.co.uk/wp-content/uploads/2025/03/Decreasing-transport-poverty-in-Europe-through-public-EV-chargepoints-March2025.pdf) в ЄС після Польщі. Частково це пов'язано з поганою інфраструктурою зарядних станцій для електромобілів у Хорватії, наприклад, зарядними станціями, які вимагають дзвінка в службу підтримки або використання декількох різних додатків для початку процесу зарядки, поганими напрямками до зарядних станцій за межами основних автомагістралей і потенційно великим часом очікування під час пікового туристичного сезону. Крім того, в Хорватії бракує надшвидкісних зарядних станцій (180 кВт і вище), що може стати проблемою для електричних вантажівок, які потребують більшої потужності, ніж середній електромобіль.

І Кіпр, і Молдова мають внутрішні геополітичні проблеми, які ускладнюють планування інфраструктури для зарядки електромобілів (як і національне планування загалом). Що стосується Кіпру, то північна половина острова, включаючи половину його столиці Нікосії, з 1974 року окупована Турецькою Республікою Північного Кіпру, яку підтримує Туреччина. Для Молдови східна провінція Придністров'я діє як де-факто держава з власним урядом. Це означає, що обидві країни не можуть послідовно впроваджувати інфраструктуру електромобілів на території, яку вони вважають своєю.

Проблеми на Кіпрі також ускладнюються високими цінами на електроенергію, тоді як Молдова має п'яту найдешевшу ціну на дизельне паливо в Європі. Молдова також є [другою найбіднішою країною в Європі] (https://worldpopulationreview.com/country-rankings/poorest-countries-in-europe), що робить інвестиції в інфраструктуру електромобілів складним завданням. Всі ці фактори сприяють загальній низькій економії витрат для електричних вантажівок.

Польща також посідає останнє місце в списку з показником економії витрат у розмірі 24,22 євро. Незважаючи на вражаюче економічне зростання та зростаючі інвестиції в інфраструктуру зарядних станцій для електромобілів, її великі розміри означають, що покриття все ще залишається проблемою в певних районах країни - хоча це, ймовірно, [зміниться в майбутньому] (https://alternative-fuels-observatory.ec.europa.eu/general-information/news/poland-launches-major-funding-programs-zero-emission-transport).

Такі країни, як Іспанія (32,20 євро), Румунія (30,62 євро) та Ірландія (30,54 євро) займають середню позицію, коли йдеться про економію витрат на електричні вантажні автомобілі. Це, ймовірно, пов'язано з тим, що в цих країнах розвивається інфраструктура зарядних станцій для електромобілів, а також середні ціни на електроенергію та дизельне паливо.

На діаграмі нижче показано 10 країн, які мають найнижчу економію витрат при використанні електричних вантажівок:

Економія витрат на електричні вантажівки у Великобританії

У Великобританії економія витрат на електромобілі становить 36,23 євро, що ставить її на 11-е місце за економією витрат на підзарядку на 100 км. Це значною мірою пов'язано з високими цінами на пальне у Великобританії, де ціни на дизельне пальне є третіми за вартістю в Європі. Хоча економія від високих цін на дизельне пальне, безумовно, сприяє високому рівню економії витрат на електромобілі у Великій Британії, вона, ймовірно, була б набагато вищою, якби електроенергія у Великій Британії не була однією з найдорожчих в Європі.

Великобританія також очікує на покращення інфраструктури зарядних станцій для електромобілів. Британська сервісна компанія Moto активно планує побудувати [15 "суперхабів" до 2027 року] (https://www.fleetnews.co.uk/news/electric-hgv-charging-superhubs-planned-for-motorway-services). Ці суперхаби можуть краще забезпечити зарядку електромобілів більш ефективно, ніж стандартні зарядні пристрої для електромобілів. Наразі на дорогах Великої Британії існує менше п'яти спеціальних зарядних пунктів для електромобілів. Оскільки [інші компанії] (https://www.fleetnews.co.uk/news/electric-hgv-charging-superhubs-planned-for-motorway-services), такі як BP Pulse та Aegis Energy, також прагнуть інвестувати, цілком ймовірно, що в найближчому майбутньому Великобританія матиме значно покращену мережу зарядних станцій для вантажівок.

Що впливає на електрифікацію вантажівок?

Наразі на електрифікацію вантажівок впливає кілька факторів, зокрема відсутність зарядної інфраструктури, тривалий час заряджання, високі початкові витрати на переобладнання електромобілів та їх обмежений запас ходу. Крім того, порівняно низька вартість і доступність дизельного палива і транспортних засобів роблять традиційні вантажні автомобілі привабливим варіантом для [операторів автопарків] (https://snapacc.com/fleet-operators/).

Однак усі ці впливи можуть відрізнятися залежно від країни, в якій працює автопарк. Наприклад, якщо ваш автопарк експлуатується лише всередині країни, наприклад, у Норвегії чи Ісландії, то він, швидше за все, зазнає меншого впливу, ніж автопарк, що працює по всій Європі або в регіонах з гіршою інфраструктурою для електромобілів, наприклад, на Балканах.

Недостатня інфраструктура зарядних станцій

Основною перешкодою для електрифікації вантажного транспорту є недостатня інфраструктура зарядних станцій для електромобілів. Це пов'язано з тим, що електромобілі потребують мегаватної зарядки, яку більшість існуючих пунктів зарядки для легкових автомобілів (стандартних електромобілів та мікроавтобусів) не підтримують.

У Європі є багато країн, яким гостро бракує такої інфраструктури, особливо на основних вантажних маршрутах і на зупинках вантажівок. Це, як правило, бідні країни Південної та Східної Європи, такі як Молдова, Грузія та Болгарія. Не випадково, що ці країни посідають останні 10 місць за економією витрат на електромобілі.

Також бувають випадки, коли зарядні станції для електромобілів існують, але вони знаходяться в районах, які просто не можуть вмістити кілька електромобілів, що заряджаються протягом ночі, через слабку місцеву електромережу. Це часто є проблемою в більш сільських і віддалених частинах Європи.

Хоча багато європейських країн планують покращити інфраструктуру для електромобілів, це все ще тривалий і дорогий процес з численними бюрократичними, логістичними та технічними перешкодами, які необхідно подолати, не кажучи вже про модернізацію навколишньої інфраструктури, наприклад, підключення до місцевих електромереж, яка також буде необхідна.

Довгий час заряджання

Електричні вантажівки заряджаються набагато довше, ніж стандартні електромобілі. Це означає, що заряджання часто має відбуватися протягом ночі. Навіть якщо можна придбати швидкі зарядні пристрої для електромобілів, процес все одно займе не кілька хвилин, як у випадку з бензиновими автомобілями, а щонайменше дві години (https://dhl-freight-connections.com/en/solutions/charging-times-for-electric-trucks-the-goal-is-less-than-30-minutes/).

Такий тривалий час заряджання може мати зворотний ефект для операторів автопарків з точки зору часу виконання замовлень. У галузі з жорсткими графіками поставок і дедлайнами це може потенційно негативно вплинути на ефективність бізнесу.

Обмежений запас ходу електричних вантажівок

Електричні вантажівки також мають відносно обмежений запас ходу порівняно з традиційними вантажними автомобілями. За даними Safety Shield, типовий електричний вантажний автомобіль може проїхати близько 300 миль на одному заряді (приблизно відстань від Лондона до Роттердама). Типовий дизельний вантажний автомобіль може проїхати до 1 000 миль на одному баку пального (приблизно відстань від Лондона до Варшави).

На пробіг електричних вантажівок також можуть більше впливати зовнішні фактори, такі як навантаження, холодна погода та рельєф місцевості. Це може призвести до занепокоєння водіїв щодо запасу ходу, які можуть частіше підзаряджатися, щоб забезпечити достатню потужність для досягнення пункту призначення. Це, в свою чергу, може призвести до затримок доставки, особливо при проїзді через країни з погано розвиненою інфраструктурою зарядки електромобілів.

Все це робить оптимізацію маршрутів життєво важливою для операторів автопарків, які планують поїздки для своїх електромобілів. Слід зазначити, що технологія акумуляторів постійно розвивається, і в найближчому майбутньому їхня ємність, а отже, і пробіг, продовжуватимуть зростати.

Високі витрати на електромобілі

Початкова вартість електромобіля є високою (зазвичай від [160 000 до 200 000 фунтів стерлінгів] (https://electriccarguide.co.uk/the-electric-hgv-guide/), порівняно з 80 000-100 000 фунтів стерлінгів для дизельних вантажівок), що потенційно може стримувати незалежних водіїв та операторів невеликих автопарків від придбання такого транспортного засобу. Це значною мірою пов'язано з вартістю технології акумуляторних батарей. Це означає, що купівля нового електричного вантажного автомобіля обійдеться дуже дорого, оскільки технологія, яка використовується в ньому, є дорожчою, ніж у дизельному вантажному автомобілі.

Високі початкові витрати на придбання електромобілів також означають, що оператори автопарків у країнах з дешевшими тарифами на електроенергію для зарядки електромобілів, таких як Норвегія, Швеція або Фінляндія, більш схильні до переобладнання, оскільки вони швидше окуплять свої інвестиції, ніж оператори автопарків у країнах з дорогою електроенергією, таких як Ірландія та Хорватія.

Ціни на електроенергію також можуть коливатися у зв'язку з різними подіями. Наприклад, за останні п'ять років ціни на електроенергію коливалися у відповідь на відкриття економік після пандемії COVID-19, а потім вторгнення Росії в Україну в 2022 році (останнє, зокрема, мало значний вплив на європейське енергопостачання). Як наслідок, ціни на електроенергію зросли майже на 30%, з 20,5 євро/кВт-год до 26,5 євро/кВт-год для середнього показника по ЄС у період після вторгнення. Однак, оскільки середній показник по ЄС зараз нижчий, ніж у 2022 році, схоже, що електричні зарядки для вантажівок продовжать своє зростання.

По всій Європі середня вартість пробігу електричного вантажного автомобіля на 100 км становить 20,51 євро - значно дешевше, ніж 51,10 євро для дизельного вантажного автомобіля на ту ж відстань.

В міру того, як ефективність підвищується, а технології акумуляторів стають все більш поширеними і дешевшими у виробництві, електромобілі також стануть більш доступними для придбання.

Дешевизна та доступність дизельного палива

Дизельне паливо все ще відіграє домінуючу роль у галузі вантажних автомобілів. Це пов'язано з тим, що дизельна інфраструктура була добре розвинена в Європі протягом десятиліть, особливо у порівнянні з електричними зарядними пристроями для вантажівок. Сумісність дизельного палива з [паливними картками] (https://snapacc.com/newsroom/fuel-cards-in-transportation-how-snap-simplifies-fleet-life/) та його відносна дешевизна також роблять його популярним серед менеджерів вантажних автопарків.

Однак, як і у випадку з електроенергією, вартість дизельного палива коливається по всьому континенту. Ось чому в таких країнах, як Молдова, Грузія та Мальта, де дизельне пальне залишається дешевим, може виявитися вигіднішим використовувати дизельні вантажівки. І навпаки, для таких країн, як Ісландія та Нідерланди, де дизельне паливо є відносно дорогим, існує більший стимул для переходу на електричні вантажівки.

Країна з дешевим пальним може також не поспішати інвестувати значні кошти в інфраструктуру електромобілів, побоюючись відштовхнути традиційні автопарки, які в результаті можуть обрати альтернативні маршрути.

Майбутнє електричних вантажівок в Європі

Електричні вантажівки - це довгострокове майбутнє автомобільних перевезень. Вони не тільки дешевші в експлуатації, але й завдяки інвестиціям у нову інфраструктуру, яка будується швидкими темпами, стануть набагато більш фінансово та стратегічно життєздатними.

Окрім економічних переваг, електричні вантажівки також важливі для досягнення екологічних цілей, таких як "Чистий нуль" (Net Zero). Оскільки традиційні вантажівки є масштабними забруднювачами, скорочення викидів завдяки електромобілям буде відчутно в більш чистому повітрі по всій Європі.

Наступні тенденції (https://snapacc.com/newsroom/the-road-ahead-for-2025-truck-industry-trends-to-expect/), схоже, вплинуть на електричні вантажівки в майбутньому:

- Smart truck parks: Truck parks in the future will evolve to better accommodate eHGVs alongside other smart technological advancements. These truck parks may include up-to-date ultra-fast charging stations, diagnostic machines, battery swap stations, and automated cleaning services, among other features.

- Increased EU regulations: Low Emission Zones (LEZs) already exist in a number of cities (e.g. Paris, Berlin, and Milan) with more European cities likely to follow suit with more stringent EU transport regulations. Fleet operators may opt for eHGVs to meet EU regulations or retrofit their HGVs with cleaner technologies, like smart tachographs.

- AI implementation: AI technology has already had a profound sustainability impact across road haulage — with applications in route optimisation, predictive maintenance, and autonomous vehicle development. Electric vehicles will likely incorporate AI to help drive sustainability in the haulage industry over the coming decades.

- Sustainability: The shift to eHGVs is part of a wider global push toward sustainable living. The effects of extreme weather, including heatwaves and floods across Europe, show no sign of slowing due to climate change. Moving to electric HGVs is one way the world is reducing its dependence on fossil fuels.

- Fuel variety: During the transition to cleaner fuel sources, there will be a variety of HGV types on the road throughout the 2030s. Many will be older diesel models, some will be electric, and others will be powered by alternative fuels such as biofuel made from renewable biomass sources.

Керуйте витратами на електричні вантажівки розумніше

За електричними вантажівками - майбутнє, в цьому мало хто сумнівається. Економічні та екологічні переваги призведуть до того, що в найближчі роки все більше операторів автопарків та водіїв перейдуть на електромобілі. Тривалість цього перехідного періоду залежатиме від того, як швидко Європа зможе розвинути свою інфраструктуру зарядних станцій для електромобілів.

Наразі існують великі ділянки континенту, де електромобілі не є життєздатними і потребують значної оптимізації маршрутів через меншу дальність пробігу. Крім того, авансові витрати можуть відлякувати незалежних водіїв та операторів невеликих автопарків.

Технології та інфраструктура будуть продовжувати вдосконалюватися, і вже зараз існують сервіси, покликані максимально спростити управління автопарками електромобілів та пов'язаними з ними витратами. Від оптимізації маршрутів та управління автопарком до карт для паркування та мийки вантажівок - SNAP робить вантажні перевезення простими.

[Підпишіться на SNAP сьогодні.] (https://snapacc.com/sign-up/)