Guest

Üzemanyag kontra töltés: Olcsóbb vagy csak zöldebb az elektromosra való átállás?

Létrehozva: 28. 07. 2025

•

Frissítve: 19. 09. 2025

A tehergépjárművek elektromos töltőállomásainak európai elterjedése átmeneti időszakot eredményezett a kontinens hatalmas úthálózatán. Sok flottaüzemeltető és járművezető számára még mindig a klasszikus dízelüzemű nehéz tehergépjárművek jelentik a választott közlekedési eszközt. Az iparág folyamatos fejlődésével azonban az elektromos tehergépkocsikra való átállás küszöbön áll.

A [flottaüzemeltetők] (https://snapacc.com/fleet-operators/) dízelről elektromosra való átállásának megvalósíthatóságának felmérése érdekében a SNAP kutatást végzett a nehéz tehergépjárművek feltöltésének és tankolásának költségeiről különböző európai áruszállítási útvonalakon. Kiszámítottuk a villamos energiával és a gázolajjal szembeni megtakarításokat euróban 100 km-enként 35 európai országban.

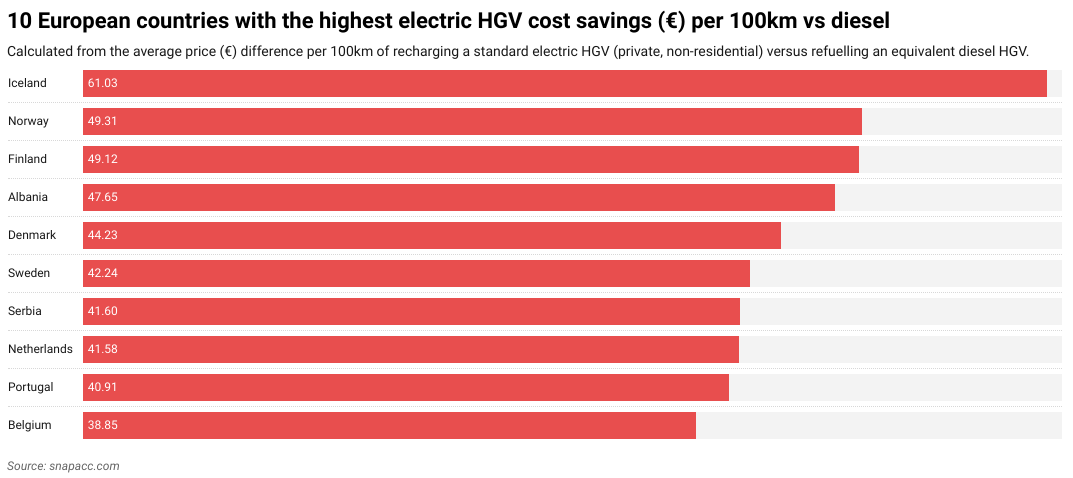

Megállapítottuk, hogy Izland áll az élen a 100 kilométerenként 61,03 EUR átlagos költségmegtakarítással, míg a második és harmadik legnagyobb költségmegtakarítást a skandináv országok, Norvégia és Finnország kínálják. A skála másik végén Horvátország kínálta a legkevesebb költségmegtakarítást (19,96 EUR/100 km), amelyet Ciprus és Moldova követett.

Ebben a cikkben feltárjuk az európai országonkénti költségmegtakarításokat, és elemezzük az európai országonkénti költségmegtakarításokat, valamint elemezzük az ezeket a megtakarításokat befolyásoló néhány külső tényezőt. Elmerülünk abban is, hogy milyen lehet az eHGV-k jövője Európában, valamint hogy az eHGV-k hogyan segíthetnek a flottaüzemeltetőknek és a járművezetőknek pénzt megtakarítani, különösen a [járművezetői költségvetésekkel] (https://snapacc.com/newsroom/a-truck-drivers-guide-to-budgeting/).

Hogyan alakulnak az eHGV és a dízel költségei az EU-ban

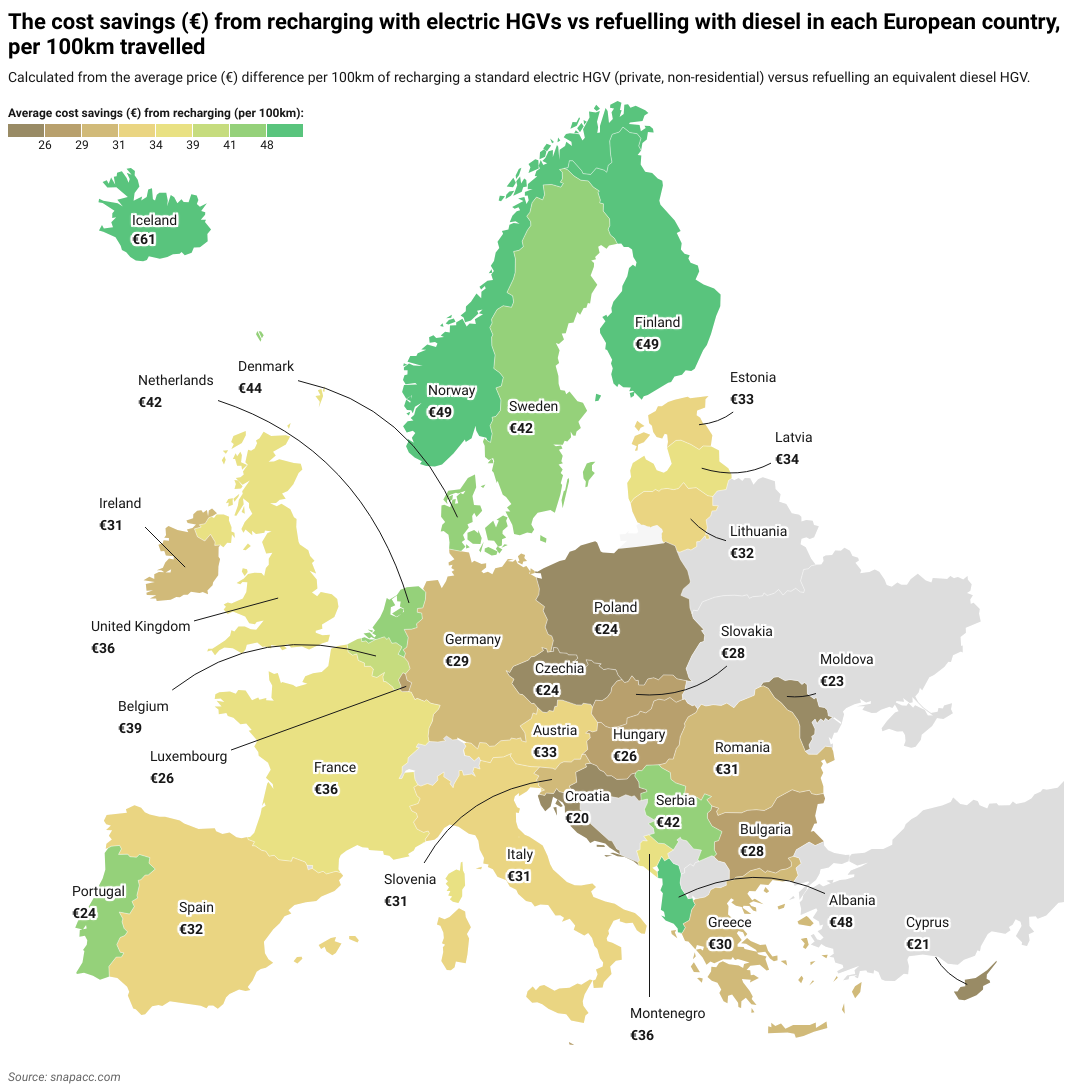

Kutatásunk megállapította, hogy minden vizsgált európai országban az elektromos töltéssel ellátott eHGV használata pénzt takarított meg a hagyományos, üzemanyaggal működő tehergépjárművek használatához képest. Az elsődleges különbség az volt, hogy a költségmegtakarítás mértéke mennyire változott. Például a legdrágább országban, Izlandban az áram ára 206%-kal magasabb (41 euróval magasabb), mint a legolcsóbb országban, Horvátországban.

Megállapítottuk, hogy egy elektromos tehergépkocsit vezető sofőr átlagosan 30,59 €/100 km megtakarítást ér el egy dízelüzemű tehergépkocsi vezetőjéhez képest. Ez a hosszú távú elektromos tehergépkocsik vezetői esetében évente átlagosan 37 200 EUR, a belföldi sofőrök esetében pedig 24 800 EUR megtakarítást jelent.

Adataink összeállításához 35 európai országot vizsgáltunk meg, és összehasonlítottuk a nehéz tehergépjárművek (HGV-k) két típusának 100 kilométerenkénti energia- vagy üzemanyagköltségét. Ezek egy standard dízelüzemű nehéz tehergépkocsi, amely 35 liter üzemanyag-fogyasztást feltételez 100 km-enként az egyes országok átlagos kiskereskedelmi dízelárával, és egy elektromos tehergépkocsi, amely 108 kWh/100 km áramfogyasztást feltételez a nem háztartási átlagos villamosenergia-tarifa alapján. A HÉA-t és a visszaigényelhető adókat nem vettük figyelembe ezekben a számításokban. Az összehasonlítás csak a közvetlen "a szivattyúnál" vagy "a konnektornál" felmerülő költségeket tükrözi, és nem veszi figyelembe az olyan tényezőket, mint a flotta mérete, a tárgyalásos energiaszerződések vagy az üzemanyag- és villamosenergia-árak jövőbeni változásai.

A gázolaj és a villamos energia árképzésének kutatásakor számos forrásból merítettünk, többek között az Eurostat, CEIC, GlobalPetrolPrices, Webfleet és Gov.uk forrásaiból. Érdemes megjegyezni, hogy e források némelyike "Nagy-Britanniára", míg mások az "Egyesült Királyságra" vonatkoznak. E kutatás céljaira a két kifejezést felcserélhetően kezelték.

Az elektromos tehergépjárművekre való átállással a legtöbbet megtakarító országok

Jelenleg Izland (61,03 EUR), Norvégia (49,31 EUR) és Finnország (49,12 EUR) azok az országok, ahol a legtöbbet lehet megtakarítani az elektromos tehergépjárművekre való átállással.

Ez nagyrészt annak köszönhető, hogy ezek az országok Európában a legdrágábbak közé tartoznak a dízelüzemanyag tekintetében. Európában Izlandon a legdrágább a gázolaj (2,07 euró/liter). Ez a meredek ár nagyrészt abból adódik, hogy Izland Európa többi részéhez képest földrajzi elszigeteltsége miatt a gázolaj importköltsége sokkal magasabb, mint más európai országoké. Izland, Norvégiához és Finnországhoz hasonlóan, magas adókulcsáról is ismert, ami szintén hozzájárul a magas üzemanyagköltségekhez.

Norvégia (32%) és Izland (18%) szintén az első két ország a világon, ahol a forgalomban lévő elektromos autók aránya a forgalomban lévő személygépkocsik között az első két helyen áll. Ennek eredményeként mindkét ország jelentős beruházásokat eszközölt az elektromos töltőinfrastruktúrába.

Izland kis mérete és fő körgyűrűje megkönnyíti az elektromos töltőállomások rendszeres időközönként történő telepítését az elektromos tehergépkocsik vezetői számára. Részben ugyanez az érvelés alkalmazható más, kisebb hálózattal rendelkező országok esetében is, amelyekben a költségmegtakarítás magas, például Albánia, Szerbia és Belgium esetében - bár meg kell jegyezni, hogy mindhárom országban az egyik legdrágábbak a gázolajárak Európában, ami hozzájárul a költségmegtakarításban mutatkozó különbséghez.

Az alábbi táblázat azt a 10 országot mutatja, ahol a legnagyobb költségmegtakarítás érhető el elektromos nehéz tehergépjárművek használata esetén:

*"A járművezetők Európa-szerte már most is megtakarításokat érnek el az elektromos tehergépkocsikra való átállással. Az eGV-töltésre való átállás az iparág jövője, és a SNAP készen áll arra, hogy segítse a járművezetőket és a flottaüzemeltetőket az átállásban." *.

Matthew Bellamy - A SNAP ügyvezető igazgatója

Az elektromos tehergépkocsikra való átállással a legkevesebbet megtakarító országok

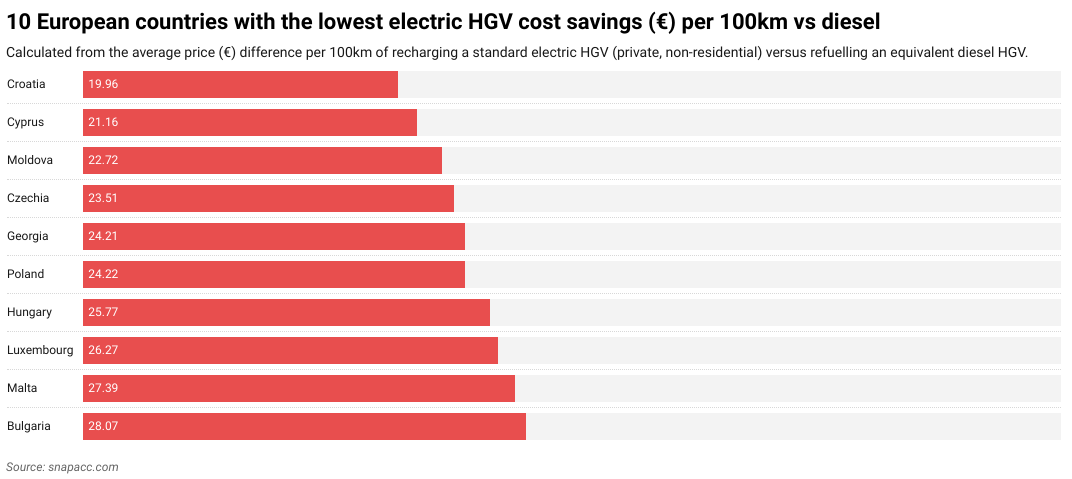

Horvátország (19,96 EUR), Ciprus (21,16 EUR) és Moldova (22,72 EUR) jelenleg a három legkevesebb költségmegtakarítást elérő ország Európában.

Lengyelország után Horvátországban [a második leglassabb az elektromos járművek elterjedtségi aránya] (https://www.smf.co.uk/wp-content/uploads/2025/03/Decreasing-transport-poverty-in-Europe-through-public-EV-chargepoints-March2025.pdf) az EU-ban. Ez részben a horvátországi EV-töltési infrastruktúra hiányosságai miatt van így: a töltőállomásokon az ügyfélszolgálatot kell felhívni, vagy több különböző alkalmazást kell használni a töltési folyamat elindításához, a főbb autópályákon kívüli töltőállomások rossz útbaigazítása, valamint a turisztikai főszezonban potenciálisan magas várakozási idő. Emellett Horvátországban nincsenek ultra-nagysebességű töltőállomások. (180 kW vagy annál nagyobb teljesítményű) töltőállomások, ami problémát jelenthet az elektromos tehergépjárművek számára, amelyeknek az átlagos EV-knél nagyobb teljesítményre van szükségük.

Cipruson és Moldovában is vannak olyan belső geopolitikai problémák, amelyek megnehezítik az elektromos járművek töltésére szolgáló infrastruktúra tervezését (és általában a nemzeti tervezést). Ciprus esetében a sziget északi felét - beleértve a főváros, Nicosia felét is - 1974 óta a török (https://www.bbc.co.uk/news/world-europe-17217956) támogatású Észak-Ciprusi Török Köztársaság [tartja megszállva]. Moldova esetében a keleti Dnyeszteren túli tartomány de facto államként működik, saját kormánnyal. Ez azt jelenti, hogy mindkét ország képtelen az EV-infrastruktúrát következetesen megvalósítani a sajátjának tekintett területen.

A ciprusi problémákat a magas villamosenergia-árak is súlyosbítják, míg Moldovában az ötödik legolcsóbb a gázolaj ára Európában. Moldova emellett [Európa második legszegényebb országa] (https://worldpopulationreview.com/country-rankings/poorest-countries-in-europe), ami kihívást jelent az EV-infrastruktúrába való beruházás szempontjából. Mindezek a tényezők hozzájárulnak ahhoz, hogy az elektromos nehéz tehergépjárművek összességében alacsony költségmegtakarítást eredményeznek.

Lengyelország szintén alacsonyan szerepel a listán 24,22 EUR költségmegtakarítással. A lenyűgöző gazdasági növekedés és az elektromos járművek töltőinfrastruktúrájába történő növekvő beruházások ellenére Lengyelország nagy mérete azt jelenti, hogy az ország egyes területein még mindig problémát jelent a lefedettség - bár ez valószínűleg [a jövőben változni fog] (https://alternative-fuels-observatory.ec.europa.eu/general-information/news/poland-launches-major-funding-programs-zero-emission-transport).

Az olyan országok, mint Spanyolország (32,20 EUR), Románia (30,62 EUR) és Írország (30,54 EUR) az út közepén helyezkednek el, amikor az elektromos nehéz tehergépjárművek költségmegtakarításáról van szó. Ez valószínűleg annak köszönhető, hogy ezekben az országokban az elektromos járművek töltési infrastruktúrája növekszik, és a villamosenergia- és gázolajköltségek közepes árúak.

Az alábbi táblázat azt a 10 országot mutatja, ahol a legalacsonyabb a költségmegtakarítás elektromos nehéz tehergépjárművek használata esetén:

Az Egyesült Királyság elektromos nehéz tehergépjárműveinek költségmegtakarítása

Az UK 36,23 EUR költségmegtakarítással rendelkezik, ami a 11. helyet jelenti a 100 kilométerenkénti feltöltésből származó költségmegtakarítás tekintetében. Ez nagyrészt annak köszönhető, hogy az Egyesült Királyságban mennyire drágák az üzemanyagárak, mivel a dízel ára a harmadik legdrágább Európában. Bár a magas dízelárakból eredő megtakarítások minden bizonnyal hozzájárulnak az Egyesült Királyság magas eHGV költségmegtakarításához, ez a megtakarítás valószínűleg sokkal magasabb lenne, ha az Egyesült Királyságban a villamos energia nem lenne a legdrágább Európában.

Az Egyesült Királyságban az EV-töltési infrastruktúra fejlesztésére is számítanak. Az Egyesült Királyság autópálya-szolgáltató vállalata, a Moto aktívan tervezi [15 "szuperközpont" építését 2027-ig] (https://www.fleetnews.co.uk/news/electric-hgv-charging-superhubs-planned-for-motorway-services). Ezek a szuperközpontok hatékonyabban tudják fogadni az eHGV-k EV-töltését, mint a hagyományos EV-töltők. Az Egyesült Királyság útjain jelenleg ötnél kevesebb eHGV-töltőpont található. Mivel [más vállalatok] (https://www.fleetnews.co.uk/news/electric-hgv-charging-superhubs-planned-for-motorway-services), mint például a BP Pulse és az Aegis Energy szintén befektetni kívánnak, valószínűsíthető, hogy az Egyesült Királyságban a közeljövőben jelentősen javuló tehergépjármű-töltőhálózat áll majd rendelkezésre.

Mi befolyásolja a nehéz tehergépjárművek villamosítását?

A nehéz tehergépjárművek villamosítását jelenleg több tényező is akadályozza, többek között a töltőinfrastruktúra hiánya, a hosszú töltési idő, az eHGV-k átalakításának magas kezdeti költségei és a korlátozott hatótávolság. Emellett a dízelüzemanyag és a járművek viszonylag alacsony ára és hozzáférhetősége miatt a hagyományos nehéz tehergépjárművek vonzó opciót jelentenek a [flottaüzemeltetők] számára.(https://snapacc.com/fleet-operators/)

Mindezek a hatások azonban a működési országtól függően változhatnak. Ha például az Ön flottája csak belföldön, például Norvégiában vagy Izlandon közlekedik, akkor valószínűleg kevésbé lesz érintett, mint egy olyan flotta, amely Európa-szerte vagy a gyengébb eHGV-infrastruktúrával rendelkező régiókban, például a Balkánon üzemel.

Elégtelen töltési infrastruktúra

A nehéz tehergépjárművek villamosításának legfőbb akadálya az eHGV töltőinfrastruktúra elégtelensége. Ennek oka, hogy az eHGV-k megawattos töltést igényelnek, amit a személygépkocsik (szabványos elektromos személygépkocsik és kisteherautók) számára a legtöbb meglévő elektromos töltőpont nem támogat.

Európában számos olyan ország van, ahol súlyos hiányosságok vannak az ilyen infrastruktúrában, különösen a főbb teherforgalmi útvonalakon és a teherautó-megállókban. Ezek általában a szegényebb dél- és kelet-európai államok, például Moldova, Grúzia és Bulgária. Nem véletlen, hogy ezek az államok az eHGV költségmegtakarítás tekintetében az utolsó 10 helyen állnak.

Az is előfordulhat, hogy léteznek ugyan eHGV töltőállomások, de olyan területeken, ahol a gyenge helyi elektromos hálózat miatt egyszerűen nem tudnak több eHGV-t éjszakai töltésre befogadni. Ez gyakran probléma Európa vidéki és távolibb részein.

Bár számos európai ország tervezi az eHGV-infrastruktúra fejlesztését, ez még mindig időigényes és költséges folyamat, amelynek számos bürokratikus, logisztikai és technikai akadályt kell leküzdenie - nem is beszélve a környező infrastruktúra-fejlesztésekről, például a helyi hálózati csatlakozásokról, amelyekre szintén szükség lesz.

Hosszú töltési idők

Az elektromos tehergépjárművek töltése sokkal hosszabb időt vesz igénybe, mint a hagyományos EV-ké. Ez azt jelenti, hogy a töltésnek gyakran éjszaka kell történnie. Még ha az eGV-gyorstöltők beszerzése lehetséges is, a folyamat akkor is [legalább két órát] (https://dhl-freight-connections.com/en/solutions/charging-times-for-electric-trucks-the-goal-is-less-than-30-minutes/) vesz igénybe, nem pedig néhány percet, mint a benzinüzemű járművek esetében.

Ez a hosszú töltési idő a flottaüzemeltetők számára az átfutási idő szempontjából is kihatással lehet. Egy olyan iparágban, ahol a szállítási ütemtervek és határidők szorosak, ez potenciálisan káros lehet az üzleti teljesítményre.

Az eHGV-k korlátozott választéka

Az elektromos tehergépkocsik hatótávolságát a hagyományos tehergépkocsik által biztosított hatótávolsághoz képest viszonylag korlátozott hatótávolságuk is korlátozza. A Safety Shield szerint egy tipikus elektromos tehergépkocsi hatótávolsága egyetlen feltöltéssel körülbelül 300 mérföld (nagyjából a London és Rotterdam közötti távolság). Egy tipikus dízelüzemű tehergépkocsi azonban akár 1 000 mérföldet is megtehet egyetlen tank üzemanyaggal (nagyjából a London és Varsó közötti távolságot).

Az elektromos nehéz tehergépjárművek futásteljesítményét külső tényezők, például a terhelés, a hideg időjárás és a terepviszonyok is jobban befolyásolhatják. Ez hatótávolsággal kapcsolatos aggodalomhoz vezethet a járművezetőknél, akik gyakrabban töltik fel a járművet, hogy biztosítsák, hogy elegendő energiával rendelkeznek az úti cél eléréséhez. Ez viszont szállítási késésekhez vezethet, különösen, ha olyan országokon keresztül vezetnek, ahol az eHGV-k töltési infrastruktúrája gyenge.

Mindezek miatt az [útvonal-optimalizálás] (https://snapacc.com/newsroom/route-optimisation-with-fleet-management-software-snap-account/) létfontosságú az eHGV-k útjait tervező flottaüzemeltetők számára. Meg kell jegyezni, hogy az akkumulátortechnológia folyamatosan fejlődik, és a kapacitás - és így a futásteljesítmény - a közeljövőben tovább fog javulni.

Magas eHGV költségek

Az eHGV kezdeti költségei magasak (jellemzően [160 000-200 000 font] (https://electriccarguide.co.uk/the-electric-hgv-guide/) között mozognak, szemben a dízel tehergépkocsik 80 000-100 000 fontjával), ami potenciálisan visszatarthatja a független járművezetőket és a kisebb flottaüzemeltetőket attól, hogy egy ilyen járművel rendelkezzenek. Ez nagyrészt az akkumulátortechnológia költségeinek köszönhető. Ez azt jelenti, hogy egy új elektromos tehergépkocsi megvásárlása költséges lesz, mivel a benne lévő technológia drágább, mint a dízel tehergépkocsiké.

A magas kezdeti eHGV beszerzési költségek azt is jelentik, hogy az olyan országokban, ahol az eHGV-töltéshez olcsóbbak az áramdíjak, mint például Norvégiában, Svédországban vagy Finnországban, a flottaüzemeltetők nagyobb valószínűséggel állnak át, mivel gyorsabban megtérül a beruházásuk, mint a drága árammal rendelkező országokban, például Írországban és Horvátországban.

A villamosenergia-árak különböző események függvényében is ingadozhatnak. Az elmúlt öt évben például a villamosenergia-árak a COVID-19 világjárványt követő gazdasági nyitásra, majd Oroszország 2022-es ukrajnai inváziójára reagálva ingadoztak (különösen az utóbbi volt jelentős hatással az európai energiaellátásra). Ennek eredményeképpen a villamosenergia-árak közel 30%-os, 20,5 c€/kWh-ról 26,5 c€/kWh-ra ugrottak meg az átlagos uniós fővárosban az inváziót követő időszakban. Mivel azonban az uniós átlag jelenleg alacsonyabb, mint 2022-ben volt, úgy tűnik, hogy a nehéz tehergépjárművek elektromos töltése tovább folytatódik.

Európa-szerte az elektromos tehergépkocsik átlagos üzemeltetési költsége 100 km-en 20,51 euró, ami lényegesen olcsóbb, mint a dízelüzemű tehergépkocsiké 51,10 euró ugyanezen a távon.

A hatékonyság javulásával és az akkumulátortechnológia elterjedésével és olcsóbbá válásával az eHGV-k beszerzése is megfizethetőbbé válik.

A dízelüzemanyag olcsósága és hozzáférhetősége

A dízelüzemanyag még mindig meghatározó szerepet játszik a nehéz tehergépjármű-iparban. Ennek oka, hogy a dízelüzemű infrastruktúra évtizedek óta jól kiépített Európában, különösen a nehéz tehergépjárművek elektromos töltőivel összehasonlítva. A dízel [üzemanyagkártyákkal] (https://snapacc.com/newsroom/fuel-cards-in-transportation-how-snap-simplifies-fleet-life/) való kompatibilitása és viszonylag olcsósága miatt is népszerű a tehergépkocsiflotta-üzemeltetők körében.

A villamos energiához hasonlóan azonban a gázolaj értéke is ingadozik az egész kontinensen. Ezért tűnhet előnyösebbnek a dízelüzemű tehergépkocsikhoz ragaszkodni olyan országokban, mint Moldova, Grúzia és Málta, ahol a gázolaj továbbra is olcsó. Ezzel szemben az olyan országok esetében, mint Izland és Hollandia, ahol a dízel viszonylag drága, nagyobb az ösztönzés az elektromos tehergépkocsira való átállásra.

Az alacsony üzemanyagköltséggel rendelkező országokban az eHGV-infrastruktúrába való erőteljes beruházástól való félelem miatt a hagyományos nehéz tehergépkocsi-flották elidegenedésétől tartva, amelyek ennek következtében alternatív útvonalakat választhatnak, szintén vonakodhatnak.

Az elektromos nehéz tehergépjárművek jövője Európában

Az elektromos tehergépkocsik jelentik a közúti áruszállítás hosszú távú jövőjét. Nemcsak hogy idővel olcsóbbak lesznek, de az új infrastruktúrába való erőteljes beruházás és építés miatt pénzügyileg és stratégiailag is sokkal életképesebbé válnak.

A gazdasági előnyökön túl az elektromos nehéz tehergépjárművek azért is fontosak, mert hozzájárulnak az olyan környezetvédelmi célokhoz, mint a Net Zero. Mivel a hagyományos tehergépkocsik nagymértékű szennyezést okoznak, az elektromos tehergépkocsik által megtakarított [kibocsátás] (https://snapacc.com/newsroom/the-road-to-sustainability-the-european-emissions-challenge-within-the-transport-sector/) az Európa-szerte tisztább levegőben fog megmutatkozni.

A [következő trendek] (https://snapacc.com/newsroom/the-road-ahead-for-2025-truck-industry-trends-to-expect/) a jövőben hatással lesznek az elektromos nehéz tehergépjárművekre:

- Smart truck parks: Truck parks in the future will evolve to better accommodate eHGVs alongside other smart technological advancements. These truck parks may include up-to-date ultra-fast charging stations, diagnostic machines, battery swap stations, and automated cleaning services, among other features.

- Increased EU regulations: Low Emission Zones (LEZs) already exist in a number of cities (e.g. Paris, Berlin, and Milan) with more European cities likely to follow suit with more stringent EU transport regulations. Fleet operators may opt for eHGVs to meet EU regulations or retrofit their HGVs with cleaner technologies, like smart tachographs.

- AI implementation: AI technology has already had a profound sustainability impact across road haulage — with applications in route optimisation, predictive maintenance, and autonomous vehicle development. Electric vehicles will likely incorporate AI to help drive sustainability in the haulage industry over the coming decades.

- Sustainability: The shift to eHGVs is part of a wider global push toward sustainable living. The effects of extreme weather, including heatwaves and floods across Europe, show no sign of slowing due to climate change. Moving to electric HGVs is one way the world is reducing its dependence on fossil fuels.

- Fuel variety: During the transition to cleaner fuel sources, there will be a variety of HGV types on the road throughout the 2030s. Many will be older diesel models, some will be electric, and others will be powered by alternative fuels such as biofuel made from renewable biomass sources.

Kezelje okosabban az eHGV költségeket

Az elektromos tehergépjárműveké a jövő, ehhez aligha fér kétség. A gazdasági és környezetvédelmi előnyök miatt az elkövetkező években egyre több flottaüzemeltető és járművezető fog átállni az eHGV-kre. Az, hogy ez az átmeneti időszak meddig tart, attól függ, hogy Európa milyen gyorsan tudja fejleszteni az eHGV töltőinfrastruktúráját.

Jelenleg a kontinens nagy része olyan terület, ahol az eHGV-k nem életképesek, és a rövidebb hatótávolságuk miatt széleskörű útvonal-optimalizálást igényelnek. Emellett a felmerülő kezdeti költségek elriaszthatják a független járművezetőket és a kisebb flottaüzemeltetőket.

A technológia és az infrastruktúra tovább fog fejlődni, és már most is léteznek olyan szolgáltatások, amelyek célja, hogy a lehető legegyszerűbbé tegyék az eHGV-flották és a kapcsolódó költségek kezelését. Az útvonal-optimalizálástól és a flottakezeléstől kezdve a parkolási térképekig és a teherautómosókig, a SNAP egyszerűvé teszi a teherautó-közlekedést.